Calculating the change in zero-coupon bonds (noun) involves determining the difference in their market values over time. For instance, if a zero-coupon bond is purchased at a price below its face value, its value will increase as it approaches maturity.

Understanding how to calculate this change is crucial for investors seeking to optimize their fixed income portfolios. The ability to accurately predict changes in zero-coupon bond values allows for informed investment decisions and effective risk management.

Historically, the development of zero-coupon bonds in the 1980s revolutionized the fixed income market. They provided investors with a new instrument for diversifying their portfolios and managing interest rate risk.

How to Calculate Change in Zero Coupon Bond

Calculating the change in zero-coupon bond values requires an understanding of several key aspects. These aspects encompass both qualitative and quantitative factors that influence the market behavior of zero-coupon bonds.

- Present Value

- Future Value

- Maturity Date

- Interest Rates

- Yield to Maturity

- Market Price

- Time Decay

- Credit Risk

- Tax Implications

Understanding the interrelationships between these aspects is crucial for accurately forecasting changes in zero-coupon bond values. For example, changes in interest rates can significantly impact the present value and future value of a zero-coupon bond. Similarly, the time to maturity and credit risk of the bond issuer influence its market price and yield to maturity. By carefully considering each of these aspects, investors can enhance their ability to make informed decisions and optimize their fixed income portfolios.

Present Value

Present Value plays a pivotal role in calculating the change in zero-coupon bond values. It represents the current worth of a future sum of money, discounted at a specified rate of return. This concept is fundamental in determining the intrinsic value of zero-coupon bonds, which pay no periodic interest payments and are sold at a discount to their face value.

- Discount Rate: The rate used to discount future cash flows back to the present value. It is typically based on the prevailing market interest rates and the creditworthiness of the bond issuer.

- Time to Maturity: The period until the bond reaches its maturity date and the investor receives the face value. Longer maturities generally result in lower present values.

- Face Value: The amount that the bondholder will receive at maturity. It represents the future value of the investment and is a key determinant of the bond’s present value.

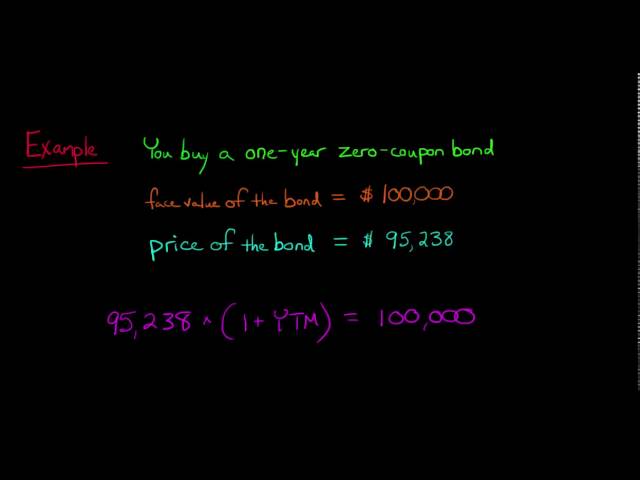

- Yield to Maturity (YTM): The internal rate of return (IRR) of the bond, calculated by equating the present value of the bond’s future cash flows to its current market price. It reflects the market’s assessment of the bond’s risk and return profile.

Understanding Present Value allows investors to assess the fair value of zero-coupon bonds and make informed decisions about buying, selling, or holding these bonds. By considering the interplay between the discount rate, time to maturity, face value, and yield to maturity, investors can effectively calculate the change in zero-coupon bond values and optimize their fixed income portfolios.

Future Value

Future Value is a crucial element in calculating the change in zero-coupon bond values. It represents the value of an investment at a specified future date, taking into account the effects of compounding interest. Understanding Future Value is essential for investors to determine the potential return on their zero-coupon bond investments and make informed decisions.

- Maturity Value: The face value of the bond, which is the amount that the bondholder will receive at maturity. It is the future value of the bond’s principal investment.

- Time to Maturity: The period until the bond reaches its maturity date. Longer maturities generally result in higher future values due to the effects of compounding interest.

- Discount Rate: The rate used to discount future cash flows back to the present value. It is typically based on the prevailing market interest rates and the creditworthiness of the bond issuer. A higher discount rate results in a lower future value.

- Yield to Maturity (YTM): The internal rate of return (IRR) of the bond, calculated by equating the present value of the bond’s future cash flows to its current market price. It reflects the market’s assessment of the bond’s risk and return profile and can be used to calculate the future value of the bond.

By considering these factors that influence Future Value, investors can accurately calculate the change in zero-coupon bond values and make informed decisions about buying, selling, or holding these bonds. Future Value provides a valuable tool for investors to assess the potential return on their investments and optimize their fixed income portfolios.

Maturity Date

The Maturity Date of a zero-coupon bond plays a critical role in calculating its change in value. It represents the specific date on which the bondholder receives the face value of the bond, marking the end of its investment term. Understanding the relationship between Maturity Date and the calculation of change in zero-coupon bond values is essential for investors.

The Maturity Date directly impacts the bond’s present value and future value, which are key factors in determining its price and yield. A longer Maturity Date typically results in a lower present value and a higher future value, as the investor has to wait longer to receive the face value. Conversely, a shorter Maturity Date leads to a higher present value and a lower future value. These relationships are crucial considerations when calculating the change in zero-coupon bond values.

In practical terms, investors use the Maturity Date to assess the potential return on their investment and make informed decisions about buying, selling, or holding zero-coupon bonds. By considering the time value of money and the impact of Maturity Date on the bond’s present and future values, investors can optimize their fixed income portfolios and achieve their financial goals.

Interest Rates

Interest Rates are a fundamental factor in calculating the change in zero-coupon bond values. They influence the present value, future value, and yield to maturity of these bonds, which are key metrics used in determining their market prices and potential returns.

- Current Market Rates: The prevailing interest rates at the time of calculation, which serve as the benchmark for discounting future cash flows and assessing the bond’s attractiveness relative to other fixed income investments.

- Discount Rate: The specific interest rate used to discount future cash flows back to the present value, typically based on the current market rates and the bond’s creditworthiness.

- Yield to Maturity (YTM): The internal rate of return (IRR) of the bond, calculated by equating the present value of the bond’s future cash flows to its current market price. Changes in interest rates can significantly impact the YTM and, consequently, the market value of the bond.

- Interest Rate Risk: The potential for changes in interest rates to affect the value of the bond. Zero-coupon bonds are particularly sensitive to interest rate risk due to their long maturities and lack of periodic interest payments.

By understanding the various facets of Interest Rates and their impact on zero-coupon bond values, investors can make informed decisions about buying, selling, or holding these bonds. Interest rate fluctuations can create opportunities for capital appreciation or losses, and investors should carefully consider their risk tolerance and investment goals before investing in zero-coupon bonds.

Yield to Maturity

Yield to Maturity (YTM) is a crucial concept in calculating the change in zero-coupon bond values. It represents the internal rate of return (IRR) of the bond, taking into account the present value of all future cash flows and the bond’s current market price. Understanding YTM is essential for investors to accurately assess the potential return on their investment and make informed decisions.

- Current Market Price: The prevailing market price of the zero-coupon bond, which directly influences the calculation of YTM. Changes in market prices can lead to changes in YTM and, consequently, the perceived value of the bond.

- Time to Maturity: The period until the bond reaches its maturity date and the investor receives the face value. Longer maturities generally result in higher YTMs, as investors require a higher return for locking their funds for a more extended period.

- Discount Rate: The rate used to discount future cash flows back to the present value, typically based on the prevailing market interest rates and the bond’s creditworthiness. Changes in discount rates can significantly impact YTM and, consequently, the market value of the bond.

- Face Value: The amount that the bondholder will receive at maturity. It represents the future value of the investment and is a key determinant of the bond’s YTM. Bonds with higher face values generally have lower YTMs, as investors are willing to accept a lower rate of return for a larger payout at maturity.

By considering these facets of YTM and its relationship to the calculation of change in zero-coupon bond values, investors can make informed decisions about buying, selling, or holding these bonds. YTM provides a comprehensive metric for assessing the potential return on investment and managing interest rate risk in fixed income portfolios.

Market Price

Market Price plays a pivotal role in calculating the change in zero-coupon bond values. It represents the current trading price of the bond in the secondary market and is influenced by various factors, each with its own implications for valuation and investment decisions.

- Supply and Demand: The balance between the number of bonds available for sale and the number of investors seeking to purchase them. Changes in supply and demand can cause market prices to fluctuate, affecting the overall value of the bond.

- Interest Rate Expectations: Market participants’ expectations about future interest rates can impact bond prices. If interest rates are expected to rise, the market price of zero-coupon bonds may decrease, as investors anticipate the availability of higher-yielding investments in the future.

- Creditworthiness of the Issuer: The financial health and creditworthiness of the entity issuing the bond can influence its market price. Bonds issued by higher-rated entities typically have lower market prices due to their lower perceived risk.

- Maturity Date: The length of time until the bond matures can also affect its market price. Generally, longer-term bonds have higher market prices due to the time value of money and the potential for interest rate fluctuations over a longer horizon.

Understanding the various facets of Market Price and their impact on zero-coupon bond values is crucial for investors. By considering these factors, investors can make informed decisions about buying, selling, or holding these bonds and effectively manage their fixed income portfolios.

Time Decay

Time Decay is an essential concept in understanding how to calculate the change in zero-coupon bond values. It refers to the decrease in the bond’s price as it approaches its maturity date. This phenomenon occurs because the present value of future cash flows decreases as the time to receive those cash flows shortens.

Time Decay is a fundamental component of how to calculate the change in zero-coupon bond values because it directly affects the bond’s present value. As the bond gets closer to maturity, its present value approaches the face value, resulting in a decrease in its market price. This relationship is particularly important for long-term zero-coupon bonds, where the impact of Time Decay can be significant.

A real-life example of Time Decay in action is the pricing of a 20-year zero-coupon bond with a face value of $1,000. Initially, the bond may trade at a significant discount to its face value, reflecting the time value of money and the uncertainty associated with such a long investment horizon. However, as the bond approaches maturity, its price will gradually increase, converging towards its $1,000 face value.

Understanding Time Decay is crucial for investors in zero-coupon bonds as it allows them to make informed decisions about buying, selling, or holding these bonds. By considering the impact of Time Decay on bond prices, investors can assess potential returns, manage interest rate risk, and optimize their fixed income portfolios.

Credit Risk

Credit Risk, an inherent element in calculating the change in zero-coupon bond values, signifies the likelihood that the bond issuer may default on its payment obligations, resulting in potential financial losses for investors. This risk assessment plays a crucial role in determining the bond’s market price and yield.

- Default Risk: The probability of the bond issuer failing to make timely interest or principal payments, leading to potential loss of invested capital.

- Downgrade Risk: The possibility of a credit rating downgrade, which can negatively impact the bond’s market value and increase its perceived risk.

- Recovery Risk: The extent to which an investor can recover their investment in the event of a default, influenced by factors such as collateral and bankruptcy laws.

- Concentration Risk: The risk associated with holding a disproportionate amount of bonds issued by a single issuer or a narrow industry sector, potentially amplifying the impact of default or downgrade.

Understanding Credit Risk and its various facets is essential for investors seeking to accurately calculate the change in zero-coupon bond values. By assessing the creditworthiness of the issuer, evaluating the potential for default or downgrade, and considering the extent of recovery and concentration risk, investors can make more informed investment decisions and manage their exposure to potential losses.

Tax Implications

Tax Implications are an integral aspect of calculating the change in zero-coupon bond values, as they can significantly impact an investor’s overall return. Understanding how taxes affect zero-coupon bonds is crucial for accurate valuation and informed investment decisions.

Zero-coupon bonds, unlike traditional coupon bonds, do not make periodic interest payments. Instead, they are issued at a discount to their face value and the investor’s return is realized upon maturity when they receive the full face value. This unique structure has specific tax implications that investors need to be aware of.

In many jurisdictions, the annual increase in the value of a zero-coupon bond is considered taxable income, even though the investor does not receive any cash payments. This means that investors may have to pay taxes on the accrued interest, even if they have not yet sold the bond or received any cash. The tax liability can be substantial, especially for long-term bonds with a high face value. It is important for investors to factor in the potential tax implications when calculating the change in zero-coupon bond values and their overall investment returns.

Frequently Asked Questions on Calculating Zero-Coupon Bond Changes

This section addresses common questions and clarifies aspects related to calculating the change in zero-coupon bond values.

Question 1: How does the maturity date impact the value of a zero-coupon bond?

Answer: The maturity date significantly influences the bond’s value. Longer maturities result in lower present values and higher future values due to the time value of money.

Question 2: What role do interest rates play in calculating zero-coupon bond changes?

Answer: Interest rates are crucial as they determine the discount rate used to calculate the present value of future cash flows. Changes in interest rates directly affect the bond’s value.

Question 3: How is the market price of a zero-coupon bond determined?

Answer: The market price reflects the present value of the bond’s future cash flows, influenced by factors like supply and demand, interest rate expectations, and the issuer’s creditworthiness.

Question 4: What is the impact of time decay on zero-coupon bond values?

Answer: Time decay refers to the decrease in bond price as it approaches maturity. This occurs because the present value of future cash flows decreases over time.

Question 5: How are taxes related to zero-coupon bonds?

Answer: In many jurisdictions, the annual increase in a zero-coupon bond’s value is taxable, even without cash payments. This can impact the investor’s overall return.

Question 6: What is the relationship between face value and zero-coupon bond value?

Answer: The face value represents the amount received at maturity. It is a key factor in determining the bond’s initial price and yield to maturity.

These FAQs provide essential insights into calculating the change in zero-coupon bond values, considering factors such as maturity, interest rates, market price, time decay, taxes, and face value. Understanding these concepts is crucial for making informed investment decisions involving zero-coupon bonds.

The next section will delve into practical strategies for effectively calculating zero-coupon bond value changes, further enhancing your understanding and enabling you to confidently navigate this aspect of fixed income investing.

Tips for Calculating Changes in Zero-Coupon Bond Values

This section provides practical tips to assist you in accurately calculating changes in zero-coupon bond values. By incorporating these tips into your investment strategy, you can make informed decisions and optimize your fixed income portfolio.

- Utilize a Bond Calculator: Leverage online or offline bond calculators to simplify the calculation process. These tools consider essential factors like maturity date, interest rates, and face value to provide accurate results.

- Consider Time Decay: Remember that zero-coupon bonds experience time decay as they approach maturity. This reduction in value should be factored into your calculations to avoid overestimating returns.

- Assess Credit Risk: Evaluate the creditworthiness of the bond issuer to determine the likelihood of default. Lower-rated bonds carry higher risk and typically offer higher yields.

- Estimate Interest Rate Sensitivity: Understand how changes in interest rates affect zero-coupon bond values. Use scenario analysis to predict potential value fluctuations under different interest rate environments.

- Factor in Tax Implications: Be aware of the tax implications associated with zero-coupon bonds in your jurisdiction. Accrued interest may be taxable, impacting your overall return.

- Monitor Market Conditions: Stay informed about economic news and market trends that can influence zero-coupon bond prices. Supply and demand dynamics, as well as macroeconomic factors, can affect bond values.

- Consult a Financial Advisor: If you need personalized guidance, consider seeking advice from a qualified financial advisor. They can help you navigate the complexities of zero-coupon bonds and develop a tailored investment strategy.

- Use Historical Data: Analyze historical bond price data to gain insights into value fluctuations and market behavior. This information can assist in making informed predictions and managing risk.

Summary: By implementing these tips, you can enhance the accuracy of your zero-coupon bond value calculations, make informed investment decisions, and mitigate potential risks. Understanding the nuances of zero-coupon bond valuation is crucial for successful fixed income investing.

Transition to Conclusion: As you progress towards the final section of this article, remember that these tips provide a solid foundation for calculating zero-coupon bond value changes effectively. In the upcoming section, we will delve into advanced strategies for optimizing your bond investments and achieving your financial goals.

Conclusion

Understanding how to calculate the change in zero-coupon bond values empowers investors to make informed decisions and optimize their fixed income portfolios. Key concepts such as present value, future value, maturity date, interest rates, yield to maturity, market price, time decay, credit risk, and tax implications all play crucial roles in determining bond values.

Accurately calculating these changes requires a comprehensive approach that considers the interconnections between these factors. By leveraging bond calculators, assessing credit risk, estimating interest rate sensitivity, factoring in tax implications, monitoring market conditions, and consulting financial advisors, investors can enhance the accuracy of their calculations and mitigate potential risks.