The calculation of coupon price, a crucial aspect of bond valuation, refers to the process of determining the current market value of a bond that pays periodic interest payments called coupons. For instance, if a bond has a face value of $1,000, a coupon rate of 5%, and 10 years remaining until maturity, its coupon price would represent the present value of the future coupon payments and the face value at maturity, discounted at the prevailing market interest rate.

Understanding how to calculate coupon price is essential for investors as it enables them to assess the fair value of bonds, make informed investment decisions, and calculate yields and returns. Historically, the advent of electronic calculators and financial software in the mid-20th century revolutionized the way coupon prices were calculated, making it an accessible task for investors of all levels.

This article will delve into the intricacies of coupon price calculation, exploring the key factors that influence it, examining different methods used for its determination, and providing insights to help investors navigate the bond market.

How to Calculate Coupon Price

Comprehending the essential aspects of coupon price calculation is pivotal for investors seeking to navigate the bond market. These key dimensions provide a framework for understanding the intricacies involved in determining the current market value of bonds.

- Face Value

- Coupon Rate

- Maturity Date

- Market Interest Rate

- Present Value

- Yield to Maturity

- Semi-Annual Payments

- Bond Rating

- Time to Maturity

The interplay of these aspects dictates the coupon price, which represents the present value of future coupon payments and the face value at maturity, discounted at the prevailing market interest rate. Understanding these key elements enables investors to assess the fair value of bonds, make informed investment decisions, and calculate yields and returns with greater precision.

Face Value

In the context of coupon price calculation, face value holds significant importance as a foundational component. Face value, also known as par value or nominal value, refers to the principal amount of a bond that is to be repaid upon maturity. It represents the amount that the issuer of the bond initially borrowed from investors and serves as a benchmark against which interest payments and the eventual repayment are calculated.

When calculating the coupon price, the face value plays a crucial role in determining the present value of the future coupon payments and the face value at maturity. The market interest rate, which is used as the discount rate in the present value calculation, is applied to the face value to determine its present value. This discounted face value, combined with the present value of the future coupon payments, gives us the coupon price.

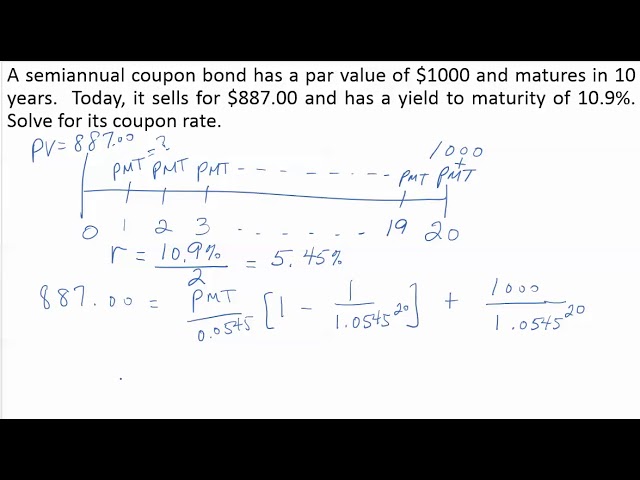

For instance, consider a bond with a face value of $1,000, a 5% coupon rate, and 10 years to maturity. If the prevailing market interest rate is 4%, the present value of the future coupon payments would be calculated as the sum of the present values of each semi-annual coupon payment (5% of $1,000 / 2 = $25) over the 10-year period, discounted at 4%. The present value of the face value at maturity would be calculated as $1,000 discounted at 4% over 10 years. The sum of these present values would give us the coupon price.

Understanding the relationship between face value and coupon price calculation is essential for investors to accurately assess the value of bonds. It enables them to compare bonds with different face values and coupon rates, and make informed decisions about which bonds to invest in based on their financial goals and risk tolerance.

Coupon Rate

In the context of “how to calculate coupon price”, coupon rate holds immense significance as a fundamental component. It directly influences the calculation of the coupon price, which is the present value of future coupon payments and the face value at maturity, discounted at the prevailing market interest rate.

A higher coupon rate leads to a higher coupon price, all other factors remaining constant. This is because a higher coupon rate means that the bond will pay more interest over its lifetime, resulting in a higher present value. Conversely, a lower coupon rate results in a lower coupon price. For instance, a bond with a 5% coupon rate will have a higher coupon price than a bond with a 3% coupon rate, assuming the same face value, maturity date, and market interest rate.

Moreover, coupon rate plays a crucial role in determining the attractiveness of a bond to investors. Bonds with higher coupon rates are generally more attractive to investors seeking higher current income, while bonds with lower coupon rates are more attractive to investors seeking capital appreciation or who anticipate future interest rate increases.

Understanding the connection between coupon rate and coupon price calculation is essential for investors to make informed decisions about bond investments. It enables them to compare bonds with different coupon rates and maturities, and assess which bonds align best with their investment goals and risk tolerance.

Maturity Date

Maturity Date holds critical importance in the calculation of coupon price, as it determines the duration over which coupon payments will be received and the face value will be repaid.

- Time to Maturity: The period between the issuance date of a bond and its maturity date. It directly influences the present value of future coupon payments and the face value at maturity, as longer maturities result in higher discounting.

- Bullet Maturity: Bonds that have a single, lump-sum payment of principal at maturity, in contrast to coupon bonds that pay interest periodically.

- Serial Maturity: Bonds that have multiple maturity dates, with different portions of the principal being repaid at specified intervals throughout the bond’s life.

- Callable Bonds: Bonds that give the issuer the option to redeem the bond before its maturity date, potentially impacting the calculation of coupon price.

Understanding the nuances of Maturity Date is crucial for investors to accurately determine the coupon price and make informed investment decisions. It enables them to assess the impact of different maturities on the present value of future cash flows and the overall attractiveness of a bond.

Market Interest Rate

In the world of fixed income securities, Market Interest Rate stands as a pivotal component of how to calculate coupon price. It exerts a profound influence on the present value of future coupon payments and, consequently, the overall coupon price of a bond.

The Market Interest Rate, often referred to as the prevailing market yield or risk-free rate, serves as the benchmark against which the present value of future cash flows is discounted. A higher Market Interest Rate leads to a lower coupon price, as the present value of future coupon payments and the face value at maturity decreases when discounted at a higher rate. Conversely, a lower Market Interest Rate results in a higher coupon price.

Understanding the relationship between Market Interest Rate and coupon price calculation is crucial for investors to make informed decisions about bond investments. It enables them to assess the impact of changing interest rates on the value of their bond holdings and to adjust their investment strategies accordingly. For instance, when Market Interest Rates are expected to rise, investors may consider investing in bonds with shorter maturities or floating coupon rates to mitigate the potential negative impact on their investments.

In conclusion, the Market Interest Rate plays a critical role in how to calculate coupon price, influencing the present value of future cash flows and the overall attractiveness of a bond investment. By understanding this relationship, investors can make informed decisions, manage risks, and optimize their bond portfolios.

Present Value

Present Value (PV) is a fundamental concept in finance that plays a critical role in the calculation of coupon prices. It refers to the current worth of a future sum of money, discounted at a specified rate of return. In the context of coupon price calculation, PV is used to determine the present value of future coupon payments, as well as the face value at maturity.

- Discount Rate: The rate of return used to discount future cash flows back to the present. It is typically the prevailing market interest rate or the yield to maturity of the bond.

- Time Value of Money: The principle that a sum of money today is worth more than the same sum in the future due to its potential earning capacity.

- Future Cash Flows: The periodic coupon payments and the face value payment at maturity that are discounted to calculate the present value.

- Compounding: The effect of earning interest on both the principal and the accumulated interest over time.

Understanding the concept of Present Value is essential for accurate coupon price calculation. It enables investors to assess the time value of money, compare bonds with different maturities and coupon rates, and make informed investment decisions. For instance, a bond with a higher present value is generally considered more valuable than a bond with a lower present value, assuming similar risk profiles.

Yield to Maturity

Yield to Maturity (YTM) holds immense significance in the realm of coupon price calculation. It represents the internal rate of return (IRR) an investor can expect to receive if they hold the bond until maturity, considering both the coupon payments and the face value repayment. Understanding YTM is paramount for investors seeking to make informed bond investment decisions.

- Market Price: The current market price of the bond, which directly influences the calculation of YTM.

- Coupon Payments: The periodic interest payments made to bondholders, which are a key component in YTM calculation.

- Maturity Date: The date on which the bond matures and the face value is repaid, marking the end of the investment period.

- Face Value: The principal amount of the bond, which is repaid to the investor at maturity and is factored into YTM calculations.

Comprehending the interplay between these facets is essential for accurate YTM calculation, which in turn enables investors to assess the attractiveness and potential returns of a bond investment. Moreover, YTM serves as a benchmark against which investors can compare different bonds and make informed decisions about their bond portfolio allocation. By considering the YTM in conjunction with other factors such as credit risk and liquidity, investors can optimize their fixed income investments and strive to achieve their financial goals.

Semi-Annual Payments

Semi-Annual Payments hold considerable significance in understanding how to calculate coupon price. They represent the practice of making interest payments on a bond in two installments per year, rather than annually or quarterly, and play a crucial role in determining the overall value and attractiveness of the bond.

- Frequency: Semi-Annual Payments divide the annual coupon payment into two equal parts, paid every six months. This more frequent payment schedule provides investors with a steady stream of income and can enhance the overall appeal of the bond.

- Calculation: The coupon price takes into account the present value of all future semi-annual payments, discounted back to the present using the prevailing market interest rate. Accrued interest is also considered, ensuring an accurate calculation of the bond’s value.

- Convenience: Semi-Annual Payments offer convenience to investors as they receive interest payments more frequently, allowing for better cash flow management and financial planning. This predictability can be particularly valuable for individuals relying on bond income.

- Yield: The yield of a bond is influenced by the frequency of coupon payments. Semi-Annual Payments generally result in a slightly higher yield compared to annual payments, as investors benefit from more frequent compounding of interest.

Understanding the implications of Semi-Annual Payments empowers investors to make informed decisions when evaluating and comparing bonds. By considering the frequency of payments, impact on yield, and overall convenience, investors can optimize their bond portfolio and achieve their financial goals.

Bond Rating

In the realm of fixed income securities, Bond Rating stands as a pivotal factor influencing the calculation of coupon prices. It serves as a concise assessment of a bond’s creditworthiness, providing investors with crucial insights into the potential risks and returns associated with the investment.

- Creditworthiness: Bond rating agencies assess the ability and willingness of the bond issuer to fulfill their financial obligations. A higher rating indicates a lower perceived risk of default, leading to a lower coupon rate and, consequently, a lower coupon price.

- Default Risk: The bond rating reflects the likelihood of the issuer defaulting on interest payments or failing to repay the principal amount at maturity. Investors use this rating to gauge the potential for financial loss and adjust their investment decisions accordingly.

- Market Perception: Bond ratings heavily influence market perception and investor demand. Bonds with higher ratings are generally considered safer and more desirable, attracting greater investor interest and potentially commanding a premium in the market.

- Pricing Impact: The bond rating directly impacts the coupon rate, which is the primary component in calculating the coupon price. A higher rating typically translates to a lower coupon rate, resulting in a lower coupon price. Conversely, a lower rating may lead to a higher coupon rate to compensate for the perceived increased risk.

Understanding the nuances of Bond Rating is essential for investors to make informed decisions about bond investments. By considering the creditworthiness, default risk, market perception, and pricing impact associated with different bond ratings, investors can effectively assess the risk-return profile of a bond and determine its suitability for their investment objectives.

Time to Maturity

In the realm of fixed income securities, “Time to Maturity” holds immense significance in understanding “how to calculate coupon price.” It represents the duration until a bond’s maturity date, the point at which the principal amount is repaid to investors. This duration directly influences the calculation of coupon price, as it determines the length of time over which interest payments are received and the present value of those payments.

The relationship between “Time to Maturity” and “how to calculate coupon price” is inversely proportional. A longer “Time to Maturity” generally leads to a lower coupon price, while a shorter “Time to Maturity” results in a higher coupon price. This is because the present value of future cash flows decreases as the time horizon increases, assuming a constant discount rate. As a result, bonds with longer maturities have a lower present value, leading to a lower coupon price.

For instance, consider two bonds with the same face value, coupon rate, and credit rating but different maturities. Bond A has a “Time to Maturity” of 5 years, while Bond B has a “Time to Maturity” of 10 years. Using the same discount rate, the present value of Bond A’s future cash flows will be higher than that of Bond B, resulting in a higher coupon price for Bond A. This demonstrates the inverse relationship between “Time to Maturity” and coupon price.

Understanding this relationship is crucial for investors to make informed bond investment decisions. By considering the “Time to Maturity” in conjunction with other factors such as coupon rate, credit rating, and market conditions, investors can assess the potential returns and risks associated with different bonds and construct a well-diversified bond portfolio that aligns with their financial goals.

FAQs on How to Calculate Coupon Price

This section addresses frequently asked questions and clarifies key aspects of calculating coupon prices, providing valuable insights to investors and individuals seeking a comprehensive understanding of this topic.

Question 1: What factors influence the calculation of coupon price?

Answer: The calculation of coupon price considers various factors, including face value, coupon rate, maturity date, market interest rate, present value, yield to maturity, semi-annual payments, bond rating, and time to maturity.

Question 2: How does coupon rate affect coupon price?

Answer: Coupon rate and coupon price have a direct relationship. A higher coupon rate leads to a higher coupon price, while a lower coupon rate results in a lower coupon price, assuming other factors remain constant.

Question 3: What role does present value play in calculating coupon price?

Answer: Present value is a crucial concept in coupon price calculation. It determines the current worth of future coupon payments and the face value at maturity, discounted at a specified rate of return.

Question 4: How does bond rating impact coupon price?

Answer: Bond rating directly affects the coupon rate, which in turn influences the coupon price. A higher bond rating typically corresponds to a lower coupon rate and, consequently, a lower coupon price, as it indicates lower perceived risk.

Question 5: Why does time to maturity affect coupon price?

Answer: Time to maturity has an inverse relationship with coupon price. Longer maturities generally lead to lower coupon prices, while shorter maturities result in higher coupon prices, as the present value of future cash flows decreases with an increasing time horizon.

Question 6: How can I calculate coupon price using these factors?

Answer: To calculate coupon price, you can use a financial calculator or employ specific formulas that incorporate the aforementioned factors. Understanding the interplay of these factors is essential for accurate coupon price calculation.

These FAQs provide a concise overview of the key aspects involved in calculating coupon prices. By grasping these concepts, individuals can develop a deeper understanding of bond valuation and make informed investment decisions.

In the following section, we will explore the practical application of these principles in determining coupon prices for different types of bonds.

Tips for Calculating Coupon Price

This section provides actionable tips to guide you in accurately calculating coupon prices. Understanding and applying these tips can enhance your bond valuation skills and support informed investment decisions.

Tip 1: Identify and gather all relevant data. Before calculating the coupon price, ensure you have the necessary information, including face value, coupon rate, maturity date, and market interest rate.

Tip 2: Determine the frequency of coupon payments. Most bonds pay coupons semi-annually, but some may have different payment schedules. Adjust your calculations accordingly.

Tip 3: Calculate the present value of each coupon payment. Discount each future coupon payment back to the present using the prevailing market interest rate.

Tip 4: Calculate the present value of the face value. Similarly, discount the face value back to the present using the market interest rate and the time remaining until maturity.

Tip 5: Sum the present values. Add the present values of all future coupon payments and the present value of the face value to obtain the coupon price.

Tip 6: Consider the impact of bond rating. Bonds with higher credit ratings typically have lower coupon rates and, therefore, lower coupon prices.

Tip 7: Understand the relationship between time to maturity and coupon price. Longer maturities generally lead to lower coupon prices due to the time value of money.

Tip 8: Use financial calculators or online tools. These resources can simplify the coupon price calculation process and minimize errors.

By following these tips, you can effectively calculate coupon prices, which are essential for evaluating bond investments, comparing different bonds, and making informed financial decisions.

The insights and practical guidance provided in this section lay the foundation for understanding the complexities of coupon price calculation. In the concluding section of this article, we will explore advanced techniques and strategies for bond valuation, building upon the knowledge gained here.

Conclusion

This comprehensive exploration of “how to calculate coupon price” has illuminated the intricacies and nuances involved in determining the present value of bonds. By understanding the key factors that influence coupon price, including face value, coupon rate, maturity date, market interest rate, and bond rating, investors can make informed decisions about bond investments.

Crucial insights gained from this article include:

- The inverse relationship between coupon rate and coupon price, with higher coupon rates leading to higher coupon prices.

- The interplay between time to maturity and coupon price, where longer maturities generally result in lower coupon prices due to the time value of money.

- The significance of bond rating in determining the perceived risk and, consequently, the coupon rate and coupon price of a bond.

As the financial landscape continues to evolve, understanding how to calculate coupon price remains essential for investors seeking to navigate the bond market effectively. By mastering these principles and staying abreast of market developments, individuals can make informed investment decisions and achieve their financial goals.