A discount bond yield to maturity formula is a calculation used to determine the annual return of a bond that is purchased below its face value. For example, a $1,000 bond that is purchased for $900 would have a discount yield to maturity of approximately 6.38%, assuming a 10-year maturity date.

The discount bond yield to maturity formula is an important tool for investors, as it allows them to compare the returns of different bonds and make informed investment decisions. Some of the key benefits of using the discount bond yield to maturity formula include its simplicity, accuracy, and universality.

The discount bond yield to maturity formula was first developed by Frederick Macaulay in 1938. Since its development, the formula has become widely used by investors and financial professionals.

In the following sections, we will discuss the discount bond yield to maturity formula in more detail, including its components, how to calculate it, and how to use it to compare different bonds.

Discount Bond Yield to Maturity Formula

The discount bond yield to maturity formula is a crucial tool for evaluating the return on a bond investment. Its key aspects encompass various dimensions, including:

- Face value

- Purchase price

- Maturity date

- Coupon payments

- Yield to maturity

- Present value

- Future value

- Time to maturity

- Discount rate

- Accrued interest

Understanding these aspects is essential for accurately calculating the yield to maturity, which represents the annualized return an investor can expect to receive if they hold the bond until maturity. The formula considers both the face value and purchase price, providing a more comprehensive assessment of the bond’s value compared to its current market price. Furthermore, it incorporates the time value of money, ensuring that the future cash flows are appropriately discounted to reflect their present worth.

Face value

The face value of a bond is the amount that the issuer of the bond promises to pay to the bondholder at maturity. It is also known as the principal or par value. The face value is typically printed on the face of the bond certificate.

The face value is an important component of the discount bond yield to maturity formula. This formula is used to calculate the annualized return on a bond that is purchased below its face value. The formula takes into account the face value, the purchase price, the maturity date, and the coupon payments.

For example, let’s say that you purchase a $1,000 bond for $900. The bond has a maturity date of 10 years and pays annual coupon payments of $50. The discount bond yield to maturity formula would be as follows:

“`YTM = (FV – PV) / (PV N)“`Where: YTM is the yield to maturity FV is the face value PV is the purchase price N is the number of years to maturityPlugging in the numbers from our example, we get:“`YTM = (1000 – 900) / (900 10) = 0.0638 or 6.38%“`This means that the annualized return on this bond is 6.38%.Understanding the relationship between face value and the discount bond yield to maturity formula is important for investors because it allows them to compare the returns of different bonds and make informed investment decisions.

Purchase price

The purchase price of a bond is the price at which an investor buys the bond. It is an important component of the discount bond yield to maturity formula, as it is used to calculate the yield to maturity (YTM). The YTM is the annualized return that an investor can expect to receive if they hold the bond until maturity.

The purchase price is inversely related to the YTM. This means that when the purchase price of a bond increases, the YTM will decrease. Conversely, when the purchase price of a bond decreases, the YTM will increase.

For example, let’s say that you purchase a $1,000 bond for $900. The bond has a maturity date of 10 years and pays annual coupon payments of $50. The YTM on this bond is 6.38%.

Now, let’s say that the price of the bond increases to $950. The YTM on the bond will now decrease to 5.73%. This is because the higher purchase price means that you are paying more for the same future cash flows. As a result, the annualized return that you can expect to receive is lower.

Understanding the relationship between the purchase price and the YTM is important for investors because it allows them to make informed investment decisions. By considering the purchase price of a bond in relation to its YTM, investors can determine which bonds offer the best returns.

Maturity date

Maturity date is a crucial aspect of the discount bond yield to maturity formula, as it marks the date on which the bond reaches its maturity. Understanding the maturity date and its implications is essential for investors to make informed decisions about bond investments.

- Timeline: The maturity date represents the end of the bond’s lifespan, after which the investor receives the face value of the bond from the issuer.

- Fixed income: Bonds are fixed-income investments, meaning that the maturity date is predetermined and fixed at the time of issuance.

- Yield to maturity: The maturity date is a critical factor in determining the yield to maturity (YTM) of a bond. The YTM represents the annualized return an investor can expect to receive if they hold the bond until maturity.

- Market value: The maturity date can influence the market value of a bond. Bonds with shorter maturities tend to be less risky and have lower yields, while bonds with longer maturities tend to be more risky and have higher yields.

In conclusion, the maturity date is a key component of the discount bond yield to maturity formula as it determines the timeline, fixed-income nature, yield to maturity, and market value of a bond. Understanding the maturity date is essential for investors to assess the risk and return profile of bond investments and make informed decisions.

Coupon Payments

Coupon payments are an integral part of the discount bond yield to maturity formula. They represent periodic interest payments made by the bond issuer to the bondholder throughout the life of the bond. These payments are crucial in determining the overall yield and return on investment for bondholders.

- Fixed Amount: Coupon payments are typically fixed and predetermined at the time of bond issuance. They are usually expressed as a percentage of the face value of the bond and paid semi-annually or annually.

- Regular Income: Coupon payments provide bondholders with a steady stream of income throughout the bond’s lifespan. This regular income can be valuable for investors seeking a stable and predictable source of cash flow.

- Impact on Yield: Coupon payments influence the yield to maturity (YTM) of a bond. Bonds with higher coupon rates tend to have lower YTMs, making them more attractive to investors seeking current income.

- Default Risk: Coupon payments are subject to default risk, meaning that the issuer may fail to make timely or full payments. This risk can impact the value of the bond and the investor’s overall return.

In conclusion, coupon payments play a significant role in the discount bond yield to maturity formula. They provide bondholders with regular income, influence the overall yield of the bond, and are subject to default risk. Understanding the nature and implications of coupon payments is crucial for investors seeking to make informed decisions about bond investments.

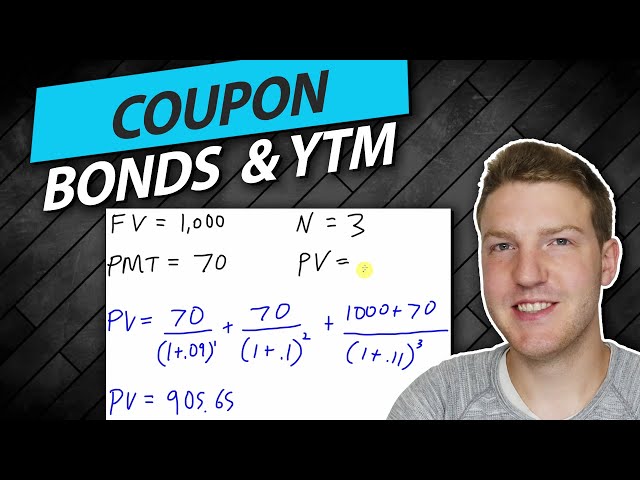

Yield to Maturity

Yield to maturity (YTM) is a critical component of the discount bond yield to maturity formula. It represents the annualized rate of return an investor can expect to receive if they hold a bond until its maturity date. YTM encompasses several key aspects that influence the overall return on investment for bondholders.

- Face Value: YTM is calculated based on the face value of the bond, which is the amount the issuer promises to repay at maturity.

- Coupon Payments: Coupon payments, which are periodic interest payments made to bondholders, are considered in the YTM calculation.

- Maturity Date: The maturity date, when the bond reaches its end, is a crucial factor in determining YTM.

- Purchase Price: The purchase price of the bond, which may be different from the face value, also impacts YTM.

In summary, YTM is a comprehensive measure that incorporates various aspects of a bond’s characteristics and cash flows to provide investors with an estimate of the potential return they can expect over the life of the investment. Understanding YTM is essential for making informed investment decisions and comparing the relative attractiveness of different bonds.

Present Value

Present value, within the context of the discount bond yield to maturity formula, plays a pivotal role in determining the current worth of future cash flows from a bond investment. It serves as a crucial factor for investors to assess the attractiveness and potential return of a bond.

- Discounted Future Cash Flows: Present value entails the process of discounting future cash flows back to their present value using a specific discount rate, which is typically the yield to maturity of the bond.

- Time Value of Money: Present value recognizes the time value of money, acknowledging that the value of a future cash flow is worth less than its face value today due to inflation and the potential for investment growth.

- Bond Pricing: The present value of the future cash flows from a bond, including coupon payments and the face value at maturity, is compared to its current market price to determine its attractiveness. This comparison helps investors make informed decisions about whether to purchase, hold, or sell a bond.

- Yield to Maturity Calculation: The yield to maturity, which represents the annualized return on a bond, is directly derived from the present value of its future cash flows. By using iterative methods, the discount rate that equates the present value of the cash flows to the current market price is determined.

In summary, present value is a critical element in the discount bond yield to maturity formula as it allows investors to evaluate the current worth of future cash flows, incorporate the time value of money, assess bond pricing, and determine the yield to maturity. Understanding the concept of present value empowers investors to make well-informed decisions about bond investments and optimize their returns.

Future value

Future value is a critical concept in the context of the discount bond yield to maturity formula, as it represents the value of a bond’s future cash flows at a specified point in time, typically its maturity date. Understanding future value is essential for investors to assess the potential return and make informed decisions about bond investments.

- Face Value: The face value of a bond is the amount that the issuer promises to repay at maturity. This represents the future value of the principal investment.

- Coupon Payments: Coupon payments are periodic interest payments made to bondholders. The future value of these payments is calculated using the time value of money and the yield to maturity.

- Maturity Date: The maturity date is the date on which the bond matures and the issuer repays the face value. The future value of the bond on this date is simply the face value.

- Yield to Maturity: The yield to maturity (YTM) is the annualized rate of return that an investor can expect to receive if they hold a bond until its maturity date. The YTM is used to discount the future cash flows back to their present value, which is then compared to the current market price of the bond.

In summary, future value is a crucial component of the discount bond yield to maturity formula as it allows investors to project the value of their investment at a specific point in time, taking into account the time value of money and the yield to maturity. By understanding the concept of future value, investors can make informed decisions about bond investments and optimize their returns.

Time to maturity

Within the context of the discount bond yield to maturity formula, time to maturity holds significant importance in determining the overall yield and attractiveness of a bond investment. It encompasses several key aspects that influence the calculation and interpretation of the yield to maturity.

- Duration: Duration measures the sensitivity of a bond’s price to changes in interest rates. Bonds with longer time to maturity tend to have higher duration, meaning their prices are more volatile in response to interest rate fluctuations.

- Maturity risk: Maturity risk refers to the potential loss of value for bonds with longer time to maturity if interest rates rise. This is because the present value of the future cash flows from these bonds decreases as interest rates increase.

- Reinvestment risk: Reinvestment risk is particularly relevant for bonds with shorter time to maturity. When these bonds mature, investors need to reinvest the proceeds at the prevailing interest rates, which may be lower than the coupon rate of the original bond.

- Call risk: Call risk applies to callable bonds, which give the issuer the option to redeem the bonds before maturity. If interest rates decline, the issuer may call the bonds, forcing investors to reinvest at lower rates.

In summary, time to maturity is a crucial factor in the discount bond yield to maturity formula as it influences the bond’s price volatility, maturity risk, reinvestment risk, and call risk. Understanding these aspects enables investors to make informed decisions about bond investments and assess the potential risks and returns associated with different maturities.

Discount rate

The discount rate plays a pivotal role in the discount bond yield to maturity formula. It represents the rate at which future cash flows are discounted to calculate the present value of a bond. The discount rate directly influences the yield to maturity (YTM), which is a crucial metric used to compare and evaluate bonds. A higher discount rate results in a lower YTM, and conversely, a lower discount rate leads to a higher YTM.

The discount rate is often determined by the prevailing market interest rates and the creditworthiness of the bond issuer. For example, bonds issued by governments or highly-rated corporations typically have lower discount rates compared to bonds issued by riskier borrowers. The choice of discount rate is critical as it affects the valuation and attractiveness of a bond investment.

In practice, the discount rate used in the discount bond yield to maturity formula is often the yield to maturity of a comparable bond with similar risk and maturity. By comparing the YTM of a bond to the YTM of a benchmark bond, investors can assess whether the bond is undervalued or overvalued.

In summary, the discount rate is a fundamental component of the discount bond yield to maturity formula. It is used to calculate the present value of future cash flows and directly impacts the yield to maturity. Understanding the relationship between the discount rate and the YTM empowers investors to make informed decisions about bond investments and assess their potential returns.

Accrued interest

Accrued interest is the interest that has been earned on a bond but has not yet been paid to the bondholder. It is an important component of the discount bond yield to maturity formula, as it affects the calculation of the bond’s yield to maturity (YTM). The YTM is the annualized rate of return that an investor can expect to receive if they hold a bond until its maturity date.

When a bond is purchased, the buyer pays the seller the bond’s price plus any accrued interest. The accrued interest is then added to the bond’s cost basis. As the bondholder holds the bond, they will receive semi-annual interest payments. These payments are typically made on January 1 and July 1. The amount of each interest payment is calculated by multiplying the bond’s coupon rate by the bond’s face value. The coupon rate is the annual interest rate that the bond pays.

If an investor sells a bond before its maturity date, they will receive the bond’s price minus any accrued interest. This is because the accrued interest has already been paid to the bondholder. The amount of accrued interest is calculated by multiplying the bond’s coupon rate by the number of days that have passed since the last interest payment date. For example, if an investor sells a bond on March 1, they will receive the bond’s price minus 61 days of accrued interest. This is because there are 61 days between January 1 and March 1.

Understanding the relationship between accrued interest and the discount bond yield to maturity formula is important for investors. This is because it allows them to calculate the YTM of a bond and to compare the YTMs of different bonds. The YTM is a valuable tool for investors, as it allows them to make informed decisions about which bonds to buy and sell.

Discount Bond Yield to Maturity Formula FAQs

This section addresses frequently asked questions (FAQs) about the discount bond yield to maturity formula. These FAQs aim to clarify common misconceptions and provide additional insights into the formula’s application and interpretation.

Question 1: What is the purpose of the discount bond yield to maturity formula?

Answer: The discount bond yield to maturity formula calculates the annualized rate of return an investor can expect to receive if they hold a bond until its maturity date. It considers the bond’s purchase price, face value, coupon payments, and time to maturity.

Question 2: How does the purchase price affect the yield to maturity?

Answer: The purchase price is inversely related to the yield to maturity. A higher purchase price results in a lower yield to maturity, as the investor pays more for the same future cash flows.

Question 3: What is the impact of coupon payments on the yield to maturity?

Answer: Coupon payments increase the yield to maturity, as they represent additional income received by the investor throughout the bond’s life.

Question 4: How does the time to maturity influence the yield to maturity?

Answer: The time to maturity is directly related to the yield to maturity. Longer maturities typically have higher yields due to increased interest rate risk and inflation uncertainty.

Question 5: What is the difference between the yield to maturity and the current yield?

Answer: The yield to maturity considers all future cash flows until the bond’s maturity, while the current yield only considers the next coupon payment and the bond’s current market price.

Question 6: How can I use the discount bond yield to maturity formula to compare different bonds?

Answer: By calculating the yield to maturity for different bonds, investors can compare their potential returns and make informed investment decisions based on their risk tolerance and investment goals.

These FAQs provide a foundational understanding of the discount bond yield to maturity formula. In the next section, we will delve deeper into the formula’s derivation and explore advanced applications in bond valuation and portfolio management.

Tips for Maximizing Bond Returns

This section provides actionable tips to help investors maximize their returns when investing in bonds. By implementing these strategies, investors can potentially enhance their portfolios and achieve their financial goals.

Tip 1: Diversify Your Bond Portfolio: Avoid concentrating your investments in a single bond or a narrow range of bonds. Diversify across different sectors, issuers, and maturities to reduce risk and improve overall portfolio performance.

Tip 2: Consider Bond Funds: Bond funds offer a convenient way to diversify your bond investments. They provide exposure to a wider range of bonds and are professionally managed, reducing the need for individual bond selection.

Tip 3: Invest in High-Quality Bonds: Prioritize bonds with high credit ratings, as they offer lower default risk and typically provide higher returns than lower-rated bonds.

Tip 4: Buy Bonds at a Discount: Look for bonds trading below their face value, as they offer the potential for capital appreciation in addition to coupon payments.

Tip 5: Hold Bonds Until Maturity: If possible, hold bonds until their maturity date to receive the full face value and avoid potential price fluctuations.

Tip 6: Monitor Interest Rate Trends: Stay informed about interest rate movements, as they can significantly impact bond prices. Consider adjusting your bond investments accordingly.

Tip 7: Seek Professional Advice: Consult with a financial advisor or investment professional for personalized guidance on bond investments. They can help you create a tailored portfolio that aligns with your specific financial goals and risk tolerance.

Summary: By following these tips, investors can enhance their bond returns, reduce risk, and potentially achieve their financial objectives. Implementing these strategies requires careful research, diversification, and monitoring, but the potential benefits can be substantial.

These tips provide a solid foundation for successful bond investing. In the next section, we will explore advanced strategies and techniques for maximizing bond returns in different market conditions.

Conclusion

In conclusion, the discount bond yield to maturity formula serves as a pivotal tool for investors seeking to evaluate and compare bond investments. This comprehensive formula incorporates various factors, including the bond’s purchase price, face value, coupon payments, time to maturity, and discount rate, to determine the annualized rate of return an investor can expect to receive if they hold the bond until maturity.

Understanding the intricacies of the formula and its underlying components empowers investors to make informed decisions about bond investments. By considering the discount bond yield to maturity in conjunction with other relevant factors, such as credit risk, market conditions, and investment goals, investors can navigate the bond market with greater confidence and potentially enhance their portfolio performance.