Determining the average coupon rate involves calculating the weighted average of the coupon rates associated with a bond’s individual payments. For instance, suppose a bond has three annual coupon payments of $5, $10, and $15, respectively. The average coupon rate would be ($5 + $10 + $15) / 3 = $10.

Calculating the average coupon rate is crucial for investors as it provides insights into the bond’s income stream and overall value. It enables comparisons between different bonds, helps assess the potential yield, and serves as a benchmark for evaluating future interest rate fluctuations. Historically, average coupon rates have been influenced by factors such as economic conditions, inflation rates, and central bank policies.

This article delves into the detailed steps involved in calculating the average coupon rate, exploring its significance in bond valuation, and examining its implications for investment decisions.

How to Calculate Average Coupon Rate

Calculating the average coupon rate is crucial for bond valuation and investment decisions. Key aspects to consider include:

- Coupon Payments

- Maturity Date

- Face Value

- Weighted Average

- Yield to Maturity

- Bond Pricing

- Investment Strategy

- Risk Assessment

Understanding these aspects provides a comprehensive framework for calculating the average coupon rate, enabling investors to make informed decisions. For instance, the weighted average calculation considers each coupon payment’s present value, while the maturity date determines the bond’s life and overall yield. Furthermore, the average coupon rate influences bond pricing, investment strategies, and risk assessments, making it a vital metric for bond investors.

Coupon Payments

Coupon payments are the regular interest payments made to bondholders throughout the life of the bond. These payments are a critical component of how to calculate average coupon rate as they represent the income generated by the bond. The average coupon rate is calculated by taking the weighted average of the coupon payments over the life of the bond, considering the time value of money.

For example, a bond with a face value of $1,000 and a 5% annual coupon rate would make semi-annual coupon payments of $25. Over a 10-year period, the bond would make 20 coupon payments totaling $500. The average coupon rate would be calculated as $500 / 20 = $25, which is equal to the face value multiplied by the annual coupon rate.

Understanding the relationship between coupon payments and how to calculate average coupon rate is essential for bond investors. The average coupon rate provides insights into the bond’s income stream and overall value, enabling comparisons between different bonds and helping investors assess the potential yield. Furthermore, the average coupon rate is a key factor in determining the bond’s price and yield to maturity, which are crucial considerations for investment decisions.

Maturity Date

Maturity date plays a crucial role in calculating the average coupon rate, determining the bond’s lifespan and overall yield. Here are four key aspects to consider:

- Bond Term: The maturity date defines the duration of the bond, influencing the calculation of the average coupon rate over its lifetime.

- Coupon Payment Frequency: Bonds with longer maturities may have different coupon payment frequencies (e.g., annual, semi-annual), affecting the calculation of the average coupon rate.

- Final Coupon Payment: The maturity date marks the final coupon payment, which may differ from regular coupon payments, impacting the average coupon rate calculation.

- Callable Bonds: Some bonds have callable features, allowing the issuer to redeem them before maturity. This can alter the calculation of the average coupon rate if the call option is exercised.

Understanding these facets of maturity date is vital for accurately calculating the average coupon rate. By considering the bond’s term, coupon payment frequency, final coupon payment, and potential call features, investors can determine the average coupon rate with greater precision. This information is essential for evaluating the bond’s value, yield, and risk profile, enabling informed investment decisions.

Face Value

Face value, also known as par value, is the nominal value of a bond, representing the amount to be repaid at maturity. It serves as a critical component in calculating the average coupon rate, which is a crucial metric for bond valuation and investment decisions.

The face value directly influences the average coupon rate calculation. The average coupon rate is determined by aggregating the present value of each coupon payment over the bond’s lifetime and dividing it by the present value of the face value received at maturity. Therefore, a higher face value leads to a lower average coupon rate, while a lower face value results in a higher average coupon rate. This inverse relationship is essential to understand for accurate bond analysis and yield calculations.

For instance, consider two bonds with identical coupon payments but different face values. Bond A has a face value of $1,000 and a 5% annual coupon rate, while Bond B has a face value of $500 and a 5% annual coupon rate. Despite having the same coupon rate, Bond A will have a lower average coupon rate due to its higher face value. This is because the present value of the face value received at maturity is greater for Bond A, resulting in a lower average coupon rate.

Understanding the connection between face value and average coupon rate is crucial for investors. It enables them to make informed decisions by considering the impact of face value on bond yield and overall return. Moreover, it helps investors compare bonds with different face values and coupon rates, facilitating effective portfolio construction and risk management.

Weighted Average

Weighted average is a fundamental concept in calculating the average coupon rate, enabling investors to accurately determine the effective yield of a bond. It involves considering the time value of money and the present value of each coupon payment over the bond’s lifetime.

The weighted average calculation assigns different weights to each coupon payment based on its timing. Coupon payments received earlier have a higher weight compared to those received later, reflecting the fact that money received today is worth more than the same amount received in the future. This weighting ensures that the average coupon rate accurately captures the bond’s true yield.

For example, consider a bond with three annual coupon payments of $50, $100, and $150, respectively. Using a weighted average, the average coupon rate would be calculated as follows:

Average Coupon Rate = [(Present Value of Coupon 1 Weight 1) + (Present Value of Coupon 2 Weight 2) + (Present Value of Coupon 3 * Weight 3)] / Present Value of Face Value

By incorporating the time value of money and assigning appropriate weights, the weighted average method provides a more accurate representation of the bond’s yield compared to a simple average. This understanding is crucial for investors to make informed decisions, compare different bonds, and assess the potential return on their investment.

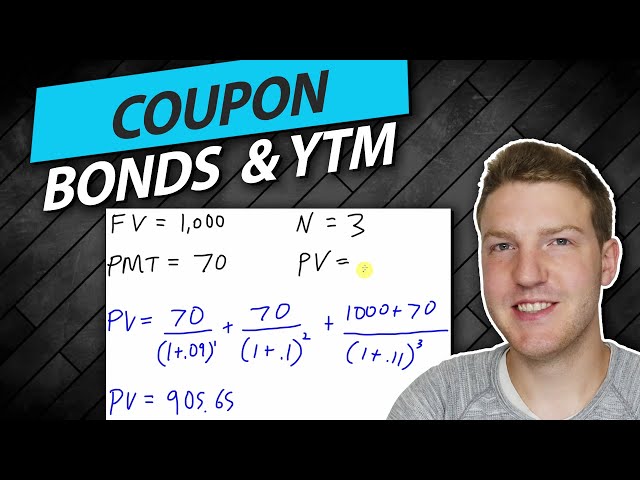

Yield to Maturity

Yield to maturity (YTM) is a critical concept closely intertwined with how to calculate average coupon rate. It represents the annualized rate of return an investor can expect to receive if they hold a bond until its maturity date. The YTM is influenced by several factors, including the bond’s coupon rate, the time remaining until maturity, and the prevailing market interest rates.

The average coupon rate plays a significant role in determining the YTM. A bond with a higher average coupon rate will generally have a higher YTM, assuming other factors remain constant. This is because the higher coupon payments result in a greater total return over the life of the bond. Conversely, a bond with a lower average coupon rate will typically have a lower YTM.

For example, consider two bonds with the same maturity date but different coupon rates. Bond A has an annual coupon rate of 5%, while Bond B has an annual coupon rate of 7%. If both bonds are priced at par, Bond B will have a higher YTM due to its higher average coupon rate.

Understanding the relationship between average coupon rate and YTM is essential for investors. It enables them to make informed decisions about which bonds to purchase based on their desired return and risk tolerance. Additionally, it helps investors compare different bonds and assess their potential value in different market conditions.

Bond Pricing

In the context of calculating the average coupon rate, bond pricing plays a pivotal role, influencing the overall yield and attractiveness of the bond. Several factors contribute to bond pricing, each carrying its own implications for investors.

- Face Value: The face value, or par value, represents the principal amount of the bond that is repaid at maturity. It serves as a reference point for calculating the average coupon rate and determines the total return on investment.

- Coupon Rate: The coupon rate, expressed as a percentage, determines the periodic interest payments made to bondholders. A higher coupon rate leads to a higher average coupon rate and, consequently, a higher bond price.

- Maturity Date: The maturity date signifies the end of the bond’s term, when the face value is repaid. Bonds with longer maturities typically have higher average coupon rates to compensate for the extended investment period.

- Market Conditions: Prevailing market conditions, such as interest rates and economic outlook, significantly impact bond pricing. Bonds are priced in relation to the prevailing yield curve, with higher interest rates leading to lower bond prices.

Understanding these facets of bond pricing is essential for investors to accurately calculate the average coupon rate and make informed investment decisions. Bond pricing provides insights into the bond’s yield, risk profile, and overall value, enabling investors to compare different bonds and construct well-diversified portfolios.

Investment Strategy

Investment strategy plays a crucial role in how to calculate average coupon rate, as it directly influences the selection and evaluation of bonds based on an investor’s financial goals and risk tolerance. Understanding this connection allows investors to make informed decisions that align with their investment objectives.

One key aspect of investment strategy is determining the desired bond duration, which affects the average coupon rate calculation. Investors seeking higher returns may opt for bonds with longer maturities and higher average coupon rates. Conversely, investors prioritizing stability and lower risk may prefer shorter-term bonds with lower average coupon rates.

Furthermore, investment strategy involves assessing the bond’s credit quality, which impacts the average coupon rate. Bonds issued by companies or governments with higher credit ratings typically have lower average coupon rates due to their lower perceived risk. Conversely, bonds with lower credit ratings often have higher average coupon rates to compensate for the increased risk.

By considering these factors within their investment strategy, investors can tailor their average coupon rate calculations to their specific goals. For instance, an investor seeking long-term growth may opt for a bond with a higher average coupon rate and longer maturity, potentially sacrificing some stability. Alternatively, an investor prioritizing capital preservation may choose a bond with a lower average coupon rate and shorter maturity, emphasizing stability over higher returns.

Risk Assessment

In the context of bond investing, risk assessment plays a pivotal role in calculating the average coupon rate and evaluating the overall attractiveness of a bond. Risk assessment involves evaluating various factors that influence the likelihood and magnitude of potential losses associated with a bond investment.

One critical aspect of risk assessment is assessing the creditworthiness of the bond issuer. This includes examining the issuer’s financial strength, stability, and ability to meet its debt obligations. Bonds issued by entities with higher credit ratings typically carry lower average coupon rates due to their lower perceived risk. Conversely, bonds issued by entities with lower credit ratings often have higher average coupon rates to compensate for the increased risk.

Furthermore, risk assessment considers market risk, which refers to the potential impact of interest rate fluctuations on the bond’s value. Bonds with longer maturities are more sensitive to interest rate changes and thus carry higher market risk. As a result, bonds with longer maturities typically have higher average coupon rates to compensate for this increased risk.

By incorporating risk assessment into the calculation of the average coupon rate, investors can gain a more comprehensive understanding of the bond’s overall investment potential. This understanding enables investors to make informed decisions and construct well-diversified portfolios that align with their risk tolerance and financial goals.

Frequently Asked Questions about Calculating Average Coupon Rate

The following FAQs address common questions and clarify aspects of calculating the average coupon rate, providing valuable insights for investors.

Question 1: What is the purpose of calculating the average coupon rate?

Answer: Calculating the average coupon rate helps investors assess the bond’s income stream, compare bonds with different coupon structures, and determine the overall yield and return on investment.

Question 2: How do I calculate the weighted average coupon rate?

Answer: The weighted average coupon rate considers the present value of each coupon payment, weighted by its time to maturity, and divides it by the present value of the face value received at maturity.

Question 3: How does the maturity date affect the average coupon rate?

Answer: The maturity date influences the calculation as it determines the lifespan of the bond and the number of coupon payments.

Question 4: What is the relationship between face value and average coupon rate?

Answer: A higher face value generally leads to a lower average coupon rate, while a lower face value results in a higher average coupon rate.

Question 5: How does the average coupon rate impact the bond’s price?

Answer: Bonds with higher average coupon rates tend to have higher prices, assuming other factors remain constant.

Question 6: How can investors use the average coupon rate in their investment strategy?

Answer: Understanding the average coupon rate can help investors make informed decisions based on their desired return and risk tolerance.

These FAQs provide a concise overview of key considerations in calculating the average coupon rate. By addressing these questions, investors gain a deeper comprehension of this important metric, enabling them to make more informed investment decisions.

To further delve into the implications of the average coupon rate, the next section explores its role in bond valuation and yield calculations.

Tips for Calculating Average Coupon Rate

To ensure accuracy and optimize investment decisions, consider the following tips when calculating the average coupon rate:

Tip 1: Verify Coupon Payment Details: Confirm the number, frequency, and amount of coupon payments to ensure an accurate calculation.

Tip 2: Consider Maturity Date: Determine the bond’s maturity date to calculate the time period over which coupon payments will be received.

Tip 3: Calculate Present Value of Face Value: Determine the present value of the face value received at maturity using the prevailing market interest rate.

Tip 4: Calculate Present Value of Each Coupon: Calculate the present value of each coupon payment using the time to maturity and the prevailing market interest rate.

Tip 5: Calculate Weighted Average: Determine the weighted average coupon rate by dividing the sum of the present value of each coupon by the present value of the face value.

Tip 6: Consider Callable Bonds: If the bond has a call feature, adjust the calculation to reflect the potential early redemption.

Tip 7: Use Financial Calculators or Spreadsheets: Leverage financial calculators or spreadsheet formulas for precise and efficient calculation.

Tip 8: Compare Different Bonds: Calculate the average coupon rate for multiple bonds to compare their yields and make informed investment choices.

By following these tips, investors can enhance the accuracy and effectiveness of their average coupon rate calculations, leading to more informed investment decisions.

In the concluding section, we will explore advanced strategies for bond valuation and yield calculations, building upon the foundation established by these tips.

Conclusion

This comprehensive guide has explored the intricacies of calculating the average coupon rate, providing valuable insights into bond valuation and yield analysis. Key points highlighted throughout the article include:

- Weighted Average: The average coupon rate is a weighted average of coupon payments, considering each payment’s present value and time to maturity.

- Bond Characteristics: Factors such as face value, maturity date, and creditworthiness significantly influence the average coupon rate.

- Investment Implications: The average coupon rate serves as a benchmark for comparing bonds, assessing yields, and making informed investment decisions.

Understanding these concepts empowers investors to accurately calculate the average coupon rate, enabling them to make strategic investment choices that align with their financial goals. As the bond market continues to evolve, staying abreast of these calculation methods will remain crucial for investors seeking optimal returns and risk management.