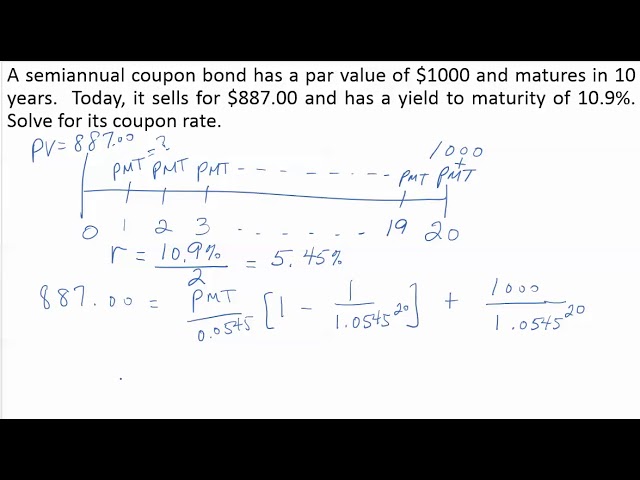

Calculating the coupon rate of a bond is a process for determining the interest rate paid by a bond issuer to bondholders over the life of the bond. This rate is expressed as a percentage of the bond’s face value.

Understanding the coupon rate is critical for bondholders as it directly impacts the return on their investment. A higher coupon rate generally indicates a higher return, making it a crucial factor in bond selection and portfolio management.

Historically, the coupon rate was determined during bond issuance and remained fixed throughout the bond’s lifespan. However, with the advent of floating-rate bonds, coupon rates can now adjust periodically, reflecting changes in prevailing interest rates and market conditions.

How to Calculate the Coupon Rate of a Bond

Calculating the coupon rate is crucial for understanding the return on investment for bondholders and plays a significant role in bond selection and portfolio management.

- Face Value

- Coupon Payment

- Bond Maturity

- Interest Rates

- Bond Pricing

- Bond Yield

- Credit Quality

- Tax Considerations

- Callable Bonds

- Floating-Rate Bonds

These aspects influence the coupon rate and provide insights into the bond’s characteristics, risk profile, and potential returns. Understanding these factors empowers investors to make informed decisions when investing in bonds.

Face Value

The face value, also known as the par value, is the principal amount of a bond, which is repaid to the bondholder at maturity. It’s a critical component in calculating the coupon rate, as it represents the base amount upon which the interest payments are determined.

The coupon rate, expressed as a percentage, is applied to the face value to calculate the periodic interest payments made to bondholders. For instance, a bond with a face value of $1,000 and a 5% coupon rate would pay an annual interest payment of $50 (1,000 x 5%).

Understanding the relationship between face value and coupon rate is crucial for bond investors as it allows them to assess the bond’s potential return and compare it to other investment options. Additionally, the face value plays a role in determining the bond’s yield-to-maturity, which is a key metric used to evaluate the overall attractiveness of the bond.

Coupon Payment

Coupon payment, an integral aspect of bond valuation, refers to the periodic interest payments made to bondholders. These payments, typically semi-annual, are calculated based on the bond’s coupon rate and face value, serving as a crucial component in deriving the overall return on investment.

- Frequency and Timing: Coupon payments are usually made at predetermined intervals, such as semi-annually or annually, with the first payment commencing after a specified grace period.

- Fixed vs. Floating: Traditionally, bonds carry fixed coupon rates, but floating-rate bonds have become increasingly common. Floating rates adjust periodically, typically pegged to a benchmark interest rate, providing flexibility in changing interest rate environments.

- Default Risk: Coupon payments are subject to the creditworthiness of the bond issuer. In the event of a default, bondholders may face delayed or missed payments, impacting their expected return.

- Tax Implications: Coupon payments are generally taxable as ordinary income, affecting the after-tax yield for bondholders. Tax-free bonds, such as municipal bonds, offer specific advantages in this regard.

Understanding the nuances of coupon payments empowers investors to make informed decisions when selecting bonds that align with their financial goals and risk tolerance. By considering the frequency, type, and potential risks associated with coupon payments, investors can effectively navigate the bond market and optimize their fixed income investments.

Bond Maturity

In the context of calculating a bond’s coupon rate, bond maturity plays a pivotal role, influencing the overall return and risk profile of the investment. It refers to the predetermined date on which the bond’s principal amount, or face value, is repaid to the bondholder.

- Term to Maturity: The period between the bond’s issuance and maturity date, which can vary from short-term (less than a year) to long-term (over 30 years).

- Callable Bonds: Bonds that grant the issuer the option to redeem them before maturity, potentially impacting the expected return and duration of the investment.

- Puttable Bonds: Bonds that allow bondholders to sell them back to the issuer before maturity, offering flexibility and potential risk mitigation strategies.

- Yield-to-Maturity: A calculation that considers the bond’s coupon payments, maturity date, and current market interest rates to determine the annualized return an investor can expect if they hold the bond until maturity.

Understanding bond maturity and its various components is essential for investors to assess the potential risks and rewards associated with different bonds. By considering the term to maturity, callable and puttable features, and the impact on yield-to-maturity, investors can make informed decisions that align with their investment goals and risk tolerance.

Interest Rates

In the context of calculating a bond’s coupon rate, interest rates play a critical role, influencing both the determination of the coupon rate and the overall attractiveness of the bond to investors. The coupon rate is directly tied to the prevailing interest rate environment, as it serves as a benchmark against which the bond’s yield is compared.

When interest rates rise, the value of existing bonds with fixed coupon rates tends to decrease. This is because investors can now purchase newly issued bonds with higher coupon rates, making the older bonds less attractive. Conversely, when interest rates fall, the value of existing bonds with fixed coupon rates tends to increase, as they offer a more favorable yield compared to new bonds with lower coupon rates.

Understanding the relationship between interest rates and the coupon rate of a bond is crucial for investors to make informed decisions when investing in fixed-income securities. By considering the current interest rate environment and the potential for future changes, investors can assess the potential risks and rewards associated with different bonds and make choices that align with their financial goals and risk tolerance.

Bond Pricing

Bond pricing is a crucial component of calculating a bond’s coupon rate and plays a significant role in determining the overall attractiveness of the bond to investors. The coupon rate is directly tied to the bond’s price, as it represents the annual interest payment made to bondholders as a percentage of the bond’s face value. When bond prices rise, the coupon rate effectively decreases, and when bond prices fall, the coupon rate increases.

In real-world scenarios, bond pricing is influenced by various factors such as interest rates, creditworthiness of the issuer, and market demand and supply. For example, if interest rates rise, the prices of existing bonds with fixed coupon rates tend to fall, as investors can now purchase newly issued bonds with higher coupon rates. Conversely, if interest rates fall, the prices of existing bonds with fixed coupon rates tend to rise, as they offer a more favorable yield compared to new bonds with lower coupon rates.

Understanding the relationship between bond pricing and the coupon rate is essential for investors to make informed decisions when investing in fixed-income securities. By considering the current bond pricing environment and the potential for future changes, investors can assess the potential risks and rewards associated with different bonds and make choices that align with their financial goals and risk tolerance.

Bond Yield

Bond yield and the calculation of a bond’s coupon rate are intertwined concepts that play a critical role in fixed-income investing. Bond yield, expressed as an annual percentage, represents the return an investor can expect to receive from a bond if held until maturity. It is a function of both the bond’s coupon rate and the bond’s price.

The coupon rate, as discussed earlier, is the fixed interest payment made to bondholders, typically semi-annually. When bond prices rise, the yield decreases, and when bond prices fall, the yield increases. This inverse relationship stems from the fact that investors are willing to pay a premium (higher price) for bonds with lower coupon rates if the prevailing interest rates are low. Conversely, if interest rates are high, investors demand higher coupon rates to compensate for the opportunity cost of investing in bonds.

Understanding the relationship between bond yield and coupon rate is crucial for investors to make informed decisions. For example, an investor seeking a higher return in a low-interest-rate environment may opt for bonds with lower coupon rates but higher bond prices, resulting in a higher yield. Conversely, in a high-interest-rate environment, investors may prefer bonds with higher coupon rates and lower bond prices, offering a more attractive yield compared to bonds with lower coupon rates.

In summary, bond yield and the calculation of a bond’s coupon rate are essential concepts for bond investors. By understanding the interplay between these factors, investors can effectively assess the risk and return characteristics of different bonds and make informed investment decisions that align with their financial goals.

Credit Quality

Credit Quality plays a pivotal role in determining a bond’s coupon rate. It assesses the borrower’s ability and willingness to make timely interest payments and repay the principal amount at maturity. Higher credit quality bonds typically carry lower coupon rates, as investors perceive them as less risky.

- Issuer Type: Government bonds generally have higher credit quality than corporate bonds, as governments are backed by the taxing power.

- Financial Health: A borrower’s financial statements and credit history provide insights into their ability to meet debt obligations.

- Industry and Economic Conditions: The industry in which a company operates and the overall economic climate can influence its creditworthiness.

- Collateral: Bonds backed by collateral, such as real estate or equipment, may have higher credit quality due to the lender’s ability to seize the assets in case of default.

Credit Quality is a crucial consideration when calculating a bond’s coupon rate. It helps investors gauge the risk associated with the investment and make informed decisions about the appropriate coupon rate to compensate for that risk.

Tax Considerations

Tax Considerations play a significant role in determining the effective return on investment for bondholders and can influence the calculation of a bond’s coupon rate. Various tax-related factors come into play, affecting the net income received by investors.

- Tax-Exempt Bonds: Interest earned on certain types of bonds, such as municipal bonds, may be exempt from federal or state income tax, making them attractive for investors seeking tax-advantaged income.

- Taxable Interest: In contrast to tax-exempt bonds, interest earned on corporate bonds and most U.S. Treasury bonds is subject to income tax, reducing the after-tax yield for investors.

- Tax-Deferred Accounts: Holding bonds in tax-deferred accounts, such as 401(k)s and IRAs, can defer tax liability on interest earnings until withdrawal, potentially enhancing returns.

- Bond Premium or Discount: When a bond is purchased at a premium (above its face value), the difference is amortized over the life of the bond, resulting in a reduction in taxable interest income. Conversely, a bond purchased at a discount leads to an increase in taxable interest income.

Understanding the tax implications associated with bonds is essential for investors to make informed decisions about their fixed-income investments. By considering the tax status of the bond’s interest payments and the potential impact on their overall financial situation, investors can effectively optimize their after-tax returns and achieve their long-term financial goals.

Callable Bonds

Callable bonds introduce an additional layer to the calculation of a bond’s coupon rate. These bonds grant the issuer the right to redeem them before their maturity date, typically at a specified call price. This feature significantly influences the bond’s yield-to-call, which is the rate of return an investor can expect if the bond is called before maturity.

When a bond is callable, the coupon rate is set with the call feature in mind. Issuers typically offer higher coupon rates on callable bonds to compensate investors for the potential risk of early redemption. However, if interest rates decline after the bond is issued, the issuer may choose to call the bond, refinancing it at a lower rate. In such scenarios, investors may not receive the full benefit of the originally stated coupon rate.

Real-life examples of callable bonds include corporate bonds issued by companies seeking to reduce their interest expenses in a favorable interest rate environment. Callable bonds can also be used by municipalities to manage their debt portfolio and take advantage of lower borrowing costs.

Understanding the impact of callable bonds on coupon rate calculations is crucial for investors. By considering the potential for early redemption and its effect on yield-to-call, investors can make informed decisions when investing in callable bonds. Additionally, it allows them to assess the trade-off between higher coupon rates and the risk of premature bond redemption.

Floating-Rate Bonds

Floating-rate bonds introduce a dynamic element to the calculation of a bond’s coupon rate. Unlike traditional fixed-rate bonds, where the coupon rate remains constant throughout the bond’s life, floating-rate bonds have coupon rates that fluctuate periodically, typically tied to a benchmark interest rate such as LIBOR or the prime rate. This unique feature makes floating-rate bonds particularly attractive in volatile interest rate environments.

The coupon rate of a floating-rate bond is calculated by adding a spread, or margin, to the reference rate. The spread compensates investors for the risk associated with the potential fluctuation in the coupon rate. As the reference rate changes, so does the coupon rate, ensuring that investors receive a consistent return above the prevailing market rate.

Real-life examples of floating-rate bonds include corporate bonds issued by companies seeking to manage their interest rate risk. Municipalities also utilize floating-rate bonds to finance infrastructure projects and other long-term capital needs while mitigating the impact of interest rate fluctuations on their budgets. Understanding the calculation of coupon rates for floating-rate bonds is essential for investors looking to diversify their portfolios and manage interest rate risk.

In summary, floating-rate bonds provide a unique way to calculate coupon rates that adapt to changing interest rate conditions. By incorporating a spread over a reference rate, investors can benefit from a variable return that adjusts to market fluctuations. This understanding is crucial for investors seeking to navigate interest rate uncertainty and achieve their financial goals.

Frequently Asked Questions on Calculating Coupon Rates of Bonds

This section addresses common questions and clarifies aspects of calculating coupon rates to enhance your understanding.

Question 1: What is the formula for calculating the coupon rate?

The coupon rate is calculated by dividing the annual coupon payment by the face value of the bond and multiplying the result by 100. The formula is: Coupon Rate = (Annual Coupon Payment Face Value) x 100

Question 2: How does bond maturity affect the coupon rate?

Bond maturity is inversely related to the coupon rate. Longer-term bonds typically offer higher coupon rates to compensate investors for the increased risk and lower liquidity associated with longer investment horizons.

Question 3: What is the impact of interest rates on coupon rates?

Interest rates and coupon rates are positively correlated. When interest rates rise, newly issued bonds offer higher coupon rates to attract investors, leading to an increase in the coupon rates of existing bonds.

Question 4: How do callable bonds affect coupon rate calculations?

Callable bonds provide issuers with the option to redeem bonds before maturity. This feature often results in higher coupon rates to compensate investors for the potential early redemption risk.

Question 5: What is the role of credit quality in determining coupon rates?

Credit quality is a crucial factor influencing coupon rates. Bonds issued by entities with higher credit ratings typically have lower coupon rates due to the lower perceived risk.

Question 6: How are coupon rates affected by tax considerations?

Tax considerations can impact the effective coupon rate for investors. Tax-exempt bonds offer lower coupon rates than taxable bonds due to the tax advantages they provide.

These FAQs provide essential insights into various aspects of calculating coupon rates. By understanding these factors, you can make informed decisions when investing in bonds and achieve your financial goals.

In the next section, we will explore advanced strategies for bond investing to enhance your portfolio performance.

Tips for Calculating Coupon Rates of Bonds

This section provides actionable tips to assist you in calculating coupon rates accurately and effectively. By incorporating these strategies into your investment process, you can enhance your bond portfolio’s performance.

Tip 1: Understand the Bond’s Face Value and Maturity Date

The face value and maturity date are crucial factors in determining the coupon rate. A bond’s face value represents the principal amount borrowed, while the maturity date indicates when the loan is due. These factors influence the bond’s overall return and risk profile.

Tip 2: Determine the Annual Coupon Payment

The annual coupon payment is the fixed interest payment made to bondholders each year. It is typically expressed as a percentage of the bond’s face value. Understanding the annual coupon payment is essential for calculating the coupon rate.

Tip 3: Use the Coupon Rate Formula

The coupon rate can be calculated using the formula: Coupon Rate = (Annual Coupon Payment / Face Value) x 100. This formula allows you to determine the coupon rate based on the bond’s face value and annual coupon payment.

Tip 4: Consider the Impact of Interest Rates

Interest rates have a significant influence on coupon rates. Rising interest rates lead to higher coupon rates on newly issued bonds, which can impact the coupon rates of existing bonds as well.

Tip 5: Factor in Credit Quality

The credit quality of the bond issuer affects the coupon rate. Bonds issued by entities with higher credit ratings typically have lower coupon rates due to the lower perceived risk.

Tip 6: Calculate Yield-to-Maturity

Yield-to-maturity (YTM) is a comprehensive measure that incorporates the bond’s coupon rate, maturity date, and current market price. It provides a more accurate assessment of the bond’s overall return potential.

Tip 7: Use Bond Pricing Tools

Various online bond pricing tools can assist you in calculating coupon rates and other bond-related metrics. These tools provide quick and convenient access to real-time bond market data.

Tip 8: Seek Professional Advice if Needed

If you are unsure about any aspect of calculating coupon rates or bond investing, do not hesitate to consult with a qualified financial advisor. They can provide personalized guidance based on your specific financial situation and goals.

Following these tips can help you navigate the complexities of calculating coupon rates and make informed decisions when investing in bonds. In the next section, we will explore essential considerations for successful bond investing.

Conclusion

In summary, calculating the coupon rate of a bond involves understanding key factors such as bond maturity, annual coupon payment, interest rates, and credit quality. The coupon rate plays a crucial role in determining the bond’s overall return and risk profile. This article has provided insights into the various aspects of coupon rate calculation, empowering readers to make informed decisions when investing in bonds.

Two main points to remember are: (1) the coupon rate is influenced by the prevailing interest rate environment and the bond’s creditworthiness; (2) factors such as bond maturity and callable features can impact the effective return on investment. Understanding these interconnections is essential for successful bond investing.