Coupon bond yield calculation, a vital financial assessment technique, determines the return on investment for fixed-income securities. Consider a 10-year bond with a $1,000 face value, a 5% annual coupon rate, and a current market price of $950. Understanding how to calculate its yield allows investors to make informed decisions.

Coupon bond yield calculation is crucial for evaluating investment opportunities, managing risk, and optimizing portfolios. Historically, the development of electronic trading platforms has made bond yield calculations more accessible and efficient, revolutionizing fixed-income investing.

This article will delve into the intricacies of coupon bond yield calculation, exploring formulas, influencing factors, and practical applications. By gaining a thorough understanding of this subject, investors can effectively navigate the bond market and achieve their financial goals.

How to Calculate Coupon Bond Yield

Understanding the essential aspects of coupon bond yield calculation is crucial for informed investment decisions. These key aspects encompass:

- Face Value

- Coupon Rate

- Market Price

- Holding Period

- Maturity Date

- Yield to Maturity

- Current Yield

- Accrued Interest

These aspects are intricately connected to the calculation of coupon bond yield. Face value represents the principal amount borrowed, while coupon rate determines the fixed interest payments. Market price reflects the current value of the bond in the secondary market, influenced by interest rate fluctuations and credit risk. Holding period and maturity date define the investment horizon and repayment timeline. Yield to maturity considers all future coupon payments and the final redemption value, providing a comprehensive measure of return. Current yield offers a snapshot of the annual return based on the current market price. Accrued interest represents the earned but unpaid interest since the last coupon payment.

Face Value

Face value, also known as par value, is the principal amount borrowed by the bond issuer and repaid at the bond’s maturity date. It serves as the foundation for calculating coupon bond yield, as it represents the reference point against which coupon payments and market price are compared.

The face value directly influences the calculation of current yield, which is the annual return based on the current market price. A higher face value, assuming other factors remain constant, leads to a lower current yield. This is because the coupon payment, which is fixed, is spread over a larger principal amount. Conversely, a lower face value results in a higher current yield.

In real-life scenarios, face value plays a crucial role in determining the bond’s overall yield and attractiveness to investors. For example, consider two bonds with the same coupon rate but different face values. The bond with a higher face value will typically have a lower current yield but may offer a higher yield to maturity if interest rates decline. This is because the larger principal amount benefits from the potential capital gain when interest rates fall.

Understanding the connection between face value and coupon bond yield empowers investors to make informed decisions about bond investments. By considering the face value in conjunction with other bond characteristics, investors can assess the potential return and risk associated with different bond offerings.

Coupon Rate

Coupon rate plays a pivotal role in the calculation of coupon bond yield. It represents the fixed percentage of the face value that is paid to bondholders as interest payments over the life of the bond. The coupon rate is a critical component of yield calculation, as it directly affects the bond’s attractiveness to investors and its overall yield. Higher coupon rates generally lead to higher yields, making bonds more appealing to income-oriented investors.

In practice, the coupon rate influences the bond’s price in the secondary market. When interest rates rise, the market value of existing bonds with lower coupon rates tends to decline, as investors can purchase newly issued bonds with higher coupon rates. Conversely, when interest rates fall, the value of bonds with higher coupon rates tends to increase, as their yields become more attractive relative to new bonds with lower coupon rates.

Understanding the relationship between coupon rate and yield is crucial for investors to make informed decisions. By considering the coupon rate in conjunction with other factors such as face value, maturity date, and credit risk, investors can assess the potential return and risk associated with different bond offerings. This understanding empowers investors to construct bond portfolios that align with their investment goals and risk tolerance.

Market Price

Market price, a pivotal aspect of coupon bond yield calculation, reflects the current value of a bond in the secondary market. It plays a crucial role in determining the bond’s yield and attractiveness to investors.

- Current Trading Price

This represents the actual price at which the bond is bought and sold in the market. It is influenced by supply and demand, interest rate fluctuations, and the bond’s credit risk.

- Clean Price

Clean price excludes accrued interest, providing a more accurate representation of the bond’s intrinsic value. It is used in yield calculations to avoid double-counting of interest.

- Dirty Price

Dirty price includes accrued interest, reflecting the total cost of purchasing the bond. It is commonly used for settlement purposes and incorporates the time value of money.

- Market Conditions

Economic conditions, interest rate expectations, and geopolitical events can influence the market price of bonds. These factors can cause price fluctuations, impacting the bond’s yield.

Understanding market price and its various components is essential for accurate coupon bond yield calculation. By considering market price in conjunction with other factors such as face value, coupon rate, and maturity date, investors can assess the potential return and risk associated with different bond offerings.

Holding Period

Holding period, a crucial aspect of coupon bond yield calculation, refers to the duration of time that an investor intends to hold a bond before selling it. It significantly influences the calculation of yield to maturity, which is a key metric for evaluating bond investments.

- Time Horizon

This encompasses the investor’s intended duration of holding the bond until maturity or sale. A longer holding period implies a greater exposure to interest rate fluctuations and market risks.

- Investment Strategy

The holding period is often aligned with the investor’s overall investment strategy. Short-term investors may hold bonds for a few months to capture short-term gains, while long-term investors may hold them for years to benefit from potential capital appreciation.

- Interest Rate Expectations

Anticipated changes in interest rates can influence the holding period. If interest rates are expected to rise, investors may prefer to hold bonds with shorter maturities to minimize potential losses. Conversely, if rates are expected to fall, they may opt for bonds with longer maturities to lock in higher yields.

- Tax Implications

In some cases, investors may adjust their holding period to optimize tax benefits. For example, holding a bond for more than a year may qualify for favorable tax treatment in certain jurisdictions.

Understanding the concept of holding period and its implications is essential for accurate coupon bond yield calculation. By considering the holding period in conjunction with other factors such as face value, coupon rate, and market price, investors can assess the potential return and risk associated with different bond offerings.

Maturity Date

Maturity date, a critical component of coupon bond yield calculation, represents the specific date on which the bond issuer repays the principal amount to bondholders. It serves as a fundamental factor in determining the bond’s yield and overall investment value.

The maturity date significantly influences the calculation of yield to maturity, a key metric used to compare different bond offerings. Yield to maturity considers the present value of all future coupon payments and the final redemption value at maturity. A longer maturity date generally leads to higher yield to maturity, as investors demand a higher return for committing their funds for an extended period.

In real-life scenarios, the maturity date plays a crucial role in investment decisions. For instance, investors seeking short-term investments with lower risk may prefer bonds with shorter maturities. Conversely, investors with a long-term investment horizon and higher risk tolerance may opt for bonds with longer maturities to lock in higher yields.

Understanding the relationship between maturity date and coupon bond yield is essential for informed investment decisions. By considering the maturity date in conjunction with other factors such as face value, coupon rate, and market price, investors can assess the potential return and risk associated with different bond offerings, enabling them to construct portfolios that align with their investment goals and risk tolerance.

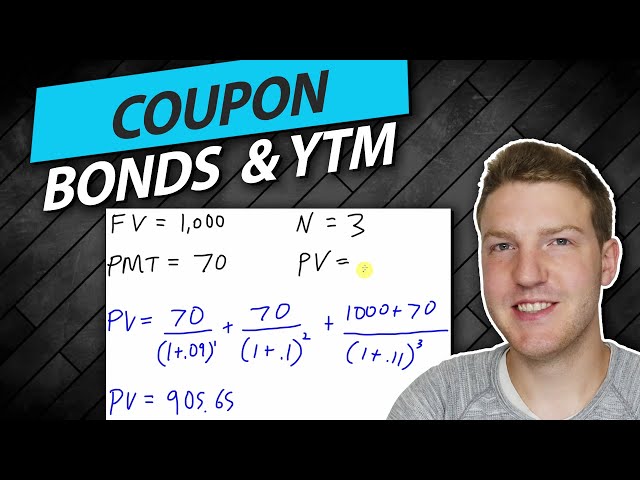

Yield to Maturity

Yield to maturity (YTM) holds a central position in the calculation of coupon bond yield. It represents the internal rate of return (IRR) that equates the present value of all future cash flows from a bond to the current market price. In essence, YTM reflects the effective annual return an investor can expect to earn by holding the bond until maturity and reinvesting all coupon payments at the same rate.

In practical terms, YTM is a critical component of coupon bond yield calculation. It provides a comprehensive measure of a bond’s return, encompassing both coupon payments and capital appreciation or depreciation at maturity. By comparing the YTM of different bonds, investors can assess their relative attractiveness and make informed investment decisions.

For example, consider two bonds with the same face value, coupon rate, and maturity date. If one bond has a higher market price than the other, its YTM will be lower. This is because the higher market price implies that investors are willing to pay more for the bond, resulting in a lower effective annual return.

Understanding the connection between yield to maturity and coupon bond yield is essential for investors to make informed decisions. By considering YTM alongside other factors such as face value, coupon rate, and maturity date, investors can assess the potential return and risk associated with different bond offerings, enabling them to construct portfolios that align with their investment goals and risk tolerance.

Current Yield

Current yield plays a significant role in the calculation of coupon bond yield, providing a snapshot of the annual return based on the current market price. It serves as a useful metric for assessing the short-term attractiveness of a bond investment.

- Annual Interest Payment

Current yield is calculated by dividing the annual interest payment by the current market price of the bond. The annual interest payment represents the fixed amount paid to bondholders each year.

- Market Price Fluctuations

Current yield is inversely related to the market price of the bond. As the market price rises, the current yield decreases, and vice versa. This relationship reflects the fact that investors demand a higher yield for bonds with lower market prices.

- Comparison of Bonds

Current yield allows investors to compare the short-term returns of different bonds. Bonds with higher current yields offer higher annual returns in the near term, while bonds with lower current yields may offer higher capital appreciation potential over the long term.

- Limitations

While current yield provides a quick assessment of a bond’s return, it has limitations. It does not consider the time value of money or the reinvestment of coupon payments, which can impact the overall yield to maturity.

Understanding the components, implications, and limitations of current yield is crucial for investors to make informed decisions. By considering current yield in conjunction with other factors such as coupon rate, maturity date, and yield to maturity, investors can assess the potential return and risk associated with different bond offerings.

Accrued Interest

Accrued interest is a crucial aspect of how to calculate coupon bond yield. It represents the interest that has been earned but not yet paid on a bond since the last coupon payment date. Understanding accrued interest is essential for accurate yield calculations and informed investment decisions.

- Calculation

Accrued interest is calculated by multiplying the bond’s annual coupon rate by the number of days that have passed since the last coupon payment date, divided by the number of days in the coupon period.

- Impact on Yield

Accrued interest affects the bond’s yield to maturity. When a bond is purchased between coupon payment dates, the investor receives the accrued interest in addition to the regular coupon payment. This increases the effective yield for the investor.

- Dirty Price

The bond’s dirty price includes accrued interest. When calculating yield, investors should use the dirty price rather than the clean price, which excludes accrued interest.

- Settlement

Accrued interest is taken into account when settling bond transactions. The buyer of a bond pays the seller the accrued interest along with the purchase price, while the seller receives the accrued interest as part of the proceeds.

In conclusion, accrued interest is an integral component of coupon bond yield calculation. It affects the effective yield for investors and must be considered when comparing bond yields and making investment decisions. Understanding accrued interest is crucial for accurate yield calculations and informed bond investing.

{FAQ

This section addresses common questions and clarifies aspects related to coupon bond yield calculation.

Question 1: What is the formula for calculating coupon bond yield?

The formula is: Yield = (Annual Coupon Payment / Current Market Price) * 100%. It expresses the bond’s annual return as a percentage.

Question 2: How does the bond’s face value affect its yield?

Face value is the principal amount borrowed. A higher face value, assuming other factors remain constant, leads to a lower current yield.

Question 3: What is the difference between yield to maturity and current yield?

Yield to maturity considers all future coupon payments and the final redemption value, while current yield provides a snapshot of the annual return based on the current market price.

Question 4: How is accrued interest treated in yield calculations?

Accrued interest increases the effective yield for the investor when a bond is purchased between coupon payment dates.

Question 5: What are the factors that influence bond yields?

Factors include interest rates, inflation, economic conditions, and the bond’s credit risk.

Question 6: How can I use yield calculations to make informed investment decisions?

By comparing yields and considering factors such as risk and investment horizon, investors can assess the potential return and risk associated with different bond offerings.

These FAQs provide a foundation for understanding coupon bond yield calculation. By addressing these questions, investors can gain a clearer perspective on this important aspect of bond investing.

Next, we will explore practical applications of coupon bond yield calculation to further enhance your understanding.

Tips for Calculating Coupon Bond Yield

This section provides actionable tips to guide you through coupon bond yield calculations:

Tip 1: Determine the annual coupon payment. Multiply the bond’s face value by its annual coupon rate.

Tip 2: Find the bond’s current market price. Check reputable financial data sources or consult with a financial advisor.

Tip 3: Calculate the current yield. Divide the annual coupon payment by the current market price and multiply by 100%.

Tip 4: Consider accrued interest. Accrued interest is the earned but unpaid interest since the last coupon payment date. It should be added to the current market price for accurate yield calculations.

Tip 5: Understand yield to maturity. Yield to maturity considers all future coupon payments and the final redemption value, providing a more comprehensive measure of return.

Tip 6: Factor in the time value of money. Consider the time value of money when comparing yields of bonds with different maturities.

Tip 7: Assess the bond’s credit risk. The creditworthiness of the bond issuer can impact its yield.

Tip 8: Use financial calculators or online tools. Various tools are available to simplify coupon bond yield calculations.

These tips empower you to calculate coupon bond yields accurately, enabling informed investment decisions. By applying these principles, you can assess the potential return and risk associated with different bond offerings.

Next, we will delve into practical examples to further solidify your understanding of coupon bond yield calculation.

Conclusion

This comprehensive analysis of coupon bond yield calculation has illuminated key aspects that empower investors to make informed decisions. Understanding the calculation process, its components, and the influencing factors is crucial for evaluating bond investments.

Key points to remember include:

- Coupon bond yield calculation involves determining the current yield, yield to maturity, and accrued interest. These metrics provide insights into the bond’s return potential and risk profile.

- Factors such as face value, coupon rate, market price, holding period, and maturity date all play a role in yield calculation. It is essential to consider these factors in conjunction to assess the overall attractiveness of a bond offering.

- Accurately calculating coupon bond yield enables investors to compare different bonds, manage their portfolios, and optimize their investment strategies.