Calculating spot rates from discount factors is a crucial financial operation that enables accurate valuation of future cash flows.

Understanding this calculation is essential for financial professionals, as it provides a precise method for determining the present value of future payments, a concept that has been employed in the financial industry for centuries.

This article will delve into the intricacies of calculating spot rates from discount factors, exploring its relevance, benefits, and key historical developments, ultimately equipping readers with the knowledge to effectively apply this essential financial tool.

How to Calculate Spot Rate from Discount Factor

Calculating spot rates from discount factors is a crucial aspect of financial analysis, as it enables the accurate valuation of future cash flows. Understanding the key aspects of this calculation is essential for financial professionals.

- Definition

- Importance

- Formula

- Applications

- Limitations

- Historical Development

- Related Concepts

- Software Tools

These aspects provide a comprehensive framework for understanding how to calculate spot rates from discount factors. By exploring each aspect in detail, financial professionals can gain a deeper insight into this essential financial tool and its applications.

Definition

Within the context of calculating spot rates from discount factors, the term “definition” encompasses several key aspects that lay the foundation for understanding this financial concept.

- Conceptual Framework

Definition establishes the theoretical underpinnings of calculating spot rates from discount factors, providing a clear understanding of the underlying principles and mathematical relationships.

- Formulaic Representation

It involves defining the mathematical formula used to calculate spot rates from discount factors, ensuring accurate and consistent calculations.

- Notational Conventions

Definition clarifies the symbols and notations used in the formula, facilitating effective communication and comprehension among financial professionals.

- Applicability and Scope

Definition outlines the specific scenarios and contexts in which calculating spot rates from discount factors is applicable, guiding users on its appropriate usage.

These facets of “definition” provide a comprehensive understanding of the concept, enabling financial professionals to grasp the theoretical underpinnings, apply the formula accurately, interpret the results effectively, and recognize the limitations and of calculating spot rates from discount factors.

Importance

The importance of calculating spot rates from discount factors lies in its fundamental role within the financial industry. Spot rates serve as crucial inputs for a wide range of financial applications, such as pricing financial instruments, managing risk, and making investment decisions.

For instance, in the foreign exchange market, calculating spot rates from discount factors enables traders to determine the current exchange rate between two currencies. This information is essential for facilitating global trade and commerce, ensuring efficient and accurate currency conversions.

Moreover, spot rates play a pivotal role in the valuation of fixed income securities, such as bonds. By calculating spot rates from discount factors, investors can assess the present value of future cash flows associated with these securities, aiding in informed investment choices.

In summary, calculating spot rates from discount factors is an indispensable skill in the financial industry. It underpins numerous financial applications, empowering professionals to make informed decisions and navigate complex financial markets effectively.

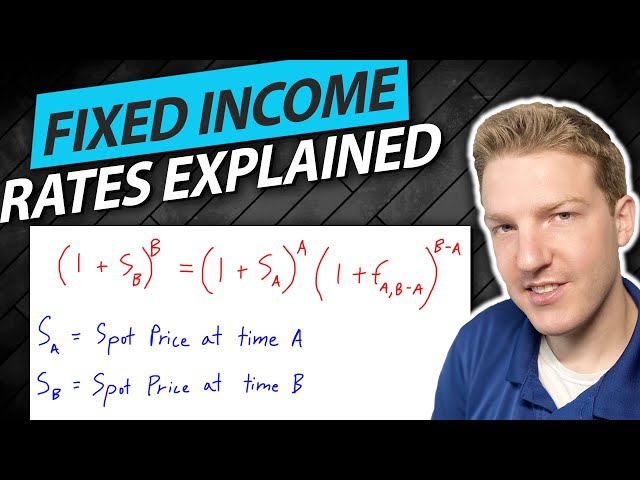

Formula

Within the context of calculating spot rates from discount factors, the formula serves as the cornerstone for accurate and consistent calculations. It establishes the precise mathematical relationship between spot rates, discount factors, and other relevant parameters.

The formula provides a step-by-step guide for financial professionals, enabling them to determine spot rates based on the available information. This is particularly crucial in complex financial markets, where accurate spot rate calculations are essential for informed decision-making.

For instance, in the foreign exchange market, the formula for calculating spot rates from discount factors empowers traders to determine the current exchange rate between two currencies, facilitating global trade and commerce. Additionally, in the fixed income market, it enables investors to assess the present value of future cash flows associated with bonds, supporting informed investment choices.

In summary, the formula for calculating spot rates from discount factors is a critical component of this financial operation, providing a precise and reliable method for determining spot rates. Its practical applications span a wide range of financial domains, empowering professionals to navigate complex markets and make informed decisions.

Applications

The applications of calculating spot rates from discount factors extend far and wide, encompassing a diverse range of financial domains. These applications are instrumental in empowering financial professionals with the tools and knowledge ncessaires to make informed decisions and navigate complex markets effectively.

- Foreign Exchange Market

In the foreign exchange market, calculating spot rates from discount factors enables traders to determine the current exchange rate between two currencies, facilitating global trade and commerce. For instance, a currency trader may use this calculation to determine the most favorable rate for converting US dollars to Euros.

- Fixed Income Market

In the fixed income market, calculating spot rates from discount factors plays a critical role in the valuation of bonds. By determining the present value of future cash flows associated with a bond, investors can make informed decisions regarding the purchase or sale of these securities.

- Risk Management

Spot rates are also essential for risk management in financial institutions. By calculating spot rates from discount factors, financial institutions can assess the potential impact of interest rate fluctuations on their portfolios and implement appropriate hedging strategies to mitigate risk.

- Financial Modeling

Calculating spot rates from discount factors is a fundamental component of financial modeling. These spot rates serve as inputs for complex financial models, enabling analysts to forecast future cash flows, assess investment opportunities, and make informed decisions.

In summary, the applications of calculating spot rates from discount factors are multifaceted and indispensable within the financial industry. These applications empower financial professionals with the necessary tools and knowledge to navigate complex markets, make informed decisions, and manage risk effectively.

Limitations

Despite its widespread applications, calculating spot rates from discount factors is not without its limitations. These limitations stem from various aspects of the calculation process and should be carefully considered when interpreting and using the results.

- Data Availability

Calculating spot rates from discount factors relies on accurate and timely data, which may not always be readily available. Factors such as market volatility and data reporting delays can introduce uncertainties into the calculation.

- Model Assumptions

The formula for calculating spot rates from discount factors relies on certain assumptions, such as the stability of interest rates and the absence of arbitrage opportunities. These assumptions may not always hold true in real-world markets, leading to potential inaccuracies in the calculated spot rates.

- Computational Complexity

Calculating spot rates from discount factors can be computationally intensive, especially for complex financial instruments or long time horizons. This can pose challenges in real-time applications or when dealing with large datasets.

- Estimation Errors

Discount factors are typically estimated using statistical models or market data. Estimation errors in these models can propagate to the calculated spot rates, potentially affecting their accuracy.

Understanding and acknowledging these limitations is crucial for financial professionals to avoid misinterpretations and make informed decisions. Despite these limitations, calculating spot rates from discount factors remains a valuable tool for financial analysis and decision-making, especially when used in conjunction with other financial models and techniques.

Historical Development

The historical development of financial markets and instruments has played a pivotal role in shaping the methods used to calculate spot rates from discount factors. Over time, advancements in financial theory and the increasing sophistication of financial markets have led to the refinement and evolution of these calculation techniques.

In the early days of financial markets, spot rates were primarily determined through informal agreements and negotiations between market participants. As markets became more complex and interconnected, the need arose for standardized and reliable methods to calculate spot rates. This led to the development of mathematical formulas and models that incorporated factors such as interest rates, time to maturity, and risk premia.

A key historical development in this regard was the introduction of discounting techniques. Discounting involves determining the present value of future cash flows by applying a discount factor that reflects the time value of money. This concept became integral to calculating spot rates, as it allowed for the valuation of future cash flows and the comparison of different investment opportunities on a consistent basis.

Today, the calculation of spot rates from discount factors is an essential component of modern financial markets. It is used in a wide range of applications, including foreign exchange trading, fixed income valuation, and risk management. The historical development of these calculation techniques has provided financial professionals with the tools and knowledge necessary to navigate complex and dynamic financial markets.

Related Concepts

Within the context of calculating spot rates from discount factors, several related concepts play a crucial role in understanding and applying this financial technique effectively. These concepts provide a comprehensive framework for analyzing the factors that influence spot rates and their implications in various financial applications.

- Discounting

Discounting involves determining the present value of future cash flows by applying a discount factor that reflects the time value of money. It is a fundamental concept in calculating spot rates, as it allows for the valuation of future cash flows and the comparison of different investment opportunities on a consistent basis.

- Forward Rates

Forward rates represent the expected future spot rates at a specified point in time. They are closely related to spot rates and are used in various financial instruments, such as forward contracts and interest rate swaps, to hedge against future interest rate movements.

- Risk-Free Rates

Risk-free rates are hypothetical rates of return that represent the return on an investment with no risk. They serve as a benchmark for assessing the risk premium associated with other investments and are used in calculating spot rates under the assumption of risk neutrality.

- Market Efficiency

Market efficiency refers to the degree to which financial markets reflect all available information. In efficient markets, spot rates are assumed to incorporate all relevant information, making it difficult to consistently outperform the market.

These related concepts provide a deeper understanding of the factors that influence spot rates and their implications in various financial applications. By considering these concepts alongside the formula and applications of calculating spot rates from discount factors, financial professionals can gain a comprehensive perspective on this essential financial technique.

Software Tools

Software tools play a vital role in facilitating the calculation of spot rates from discount factors. They provide efficient and accurate methods for performing complex calculations, enabling financial professionals to save time and minimize errors.

- Automated Calculations

Software tools automate the calculation process, eliminating the need for manual calculations and reducing the risk of errors. They can quickly and accurately calculate spot rates for various currencies and time horizons, ensuring consistency and reliability.

- Data Integration

Software tools can integrate with data sources to retrieve real-time market data. This eliminates the need for manual data input and ensures that calculations are based on the latest available information, improving the accuracy and timeliness of spot rate calculations.

- Scenario Analysis

Software tools enable users to perform scenario analysis by allowing them to easily adjust input parameters and observe the impact on spot rates. This helps financial professionals assess the sensitivity of spot rates to changes in underlying factors, such as interest rates and market conditions.

- Visualization and Reporting

Software tools offer visualization and reporting features that enable users to present their results in a clear and concise manner. They can generate charts, graphs, and tables that illustrate the relationship between spot rates and other relevant factors, facilitating analysis and communication.

In summary, software tools are invaluable aids in calculating spot rates from discount factors. They automate calculations, integrate data, enable scenario analysis, and provide visualization and reporting capabilities, enhancing the efficiency, accuracy, and comprehensiveness of the calculation process.

Frequently Asked Questions

This section addresses common questions and clarifications regarding the calculation of spot rates from discount factors, providing concise and informative answers to assist readers in fully understanding the concept and its applications.

Question 1: What is the significance of calculating spot rates from discount factors?

Answer: Calculating spot rates from discount factors enables financial professionals to determine the current value of future cash flows, which is essential for accurate valuation of financial instruments, risk management, and informed investment decisions.

Question 2: How does the formula for calculating spot rates from discount factors work?

Answer: The formula involves multiplying the future value of a cash flow by the discount factor corresponding to the time period between the present and the future date. This calculation effectively converts the future value to its present value, providing the spot rate.

Question 3: What factors influence the spot rate calculated from a discount factor?

Answer: Spot rates are primarily influenced by the prevailing interest rates, the time to maturity of the cash flow, and the risk associated with the underlying financial instrument.

Question 4: How can I apply the calculated spot rate in practical financial scenarios?

Answer: Spot rates are used in various financial applications, such as foreign exchange trading to determine currency exchange rates and in fixed income markets to value bonds and assess their yield.

Question 5: What are some common challenges or limitations in calculating spot rates from discount factors?

Answer: Challenges include data availability, estimation errors in discount factors, and the need for accurate assumptions about future interest rates.

Question 6: How can I enhance the accuracy of spot rate calculations from discount factors?

Answer: To improve accuracy, consider using reliable data sources, employing robust estimation techniques for discount factors, and incorporating scenario analysis to assess the impact of varying interest rate assumptions.

These FAQs provide a concise overview of the key aspects of calculating spot rates from discount factors. By addressing common questions and clarifying important concepts, they aim to enhance readers’ understanding and equip them with a solid foundation for further exploration of this topic.

The next section delves deeper into the intricacies of calculating spot rates from discount factors, exploring advanced techniques and applications in various financial domains.

Tips for Calculating Spot Rates from Discount Factors

This section provides a comprehensive guide to calculating spot rates from discount factors, empowering financial professionals with practical tips and techniques to enhance their accuracy and efficiency in this critical financial operation.

Utilize Reliable Data Sources: Ensure access to accurate and timely market data to minimize errors and ensure the robustness of your calculations.

Employ Robust Estimation Techniques: Use sophisticated models and statistical methods to estimate discount factors, mitigating potential estimation biases and improving the reliability of your spot rate calculations.

Incorporate Scenario Analysis: Analyze the impact of varying interest rate assumptions on spot rates through scenario analysis, providing a comprehensive understanding of potential outcomes.

Leverage Technology and Automation: Utilize software tools and platforms to automate calculations, reduce errors, and save time, allowing you to focus on strategic analysis.

Stay Updated with Market Trends: Continuously monitor market developments and economic indicators to stay abreast of factors that influence spot rates, enabling informed decision-making.

Consider Market Efficiency: Assess the efficiency of the financial markets to understand the potential limitations of spot rate calculations and make informed judgments.

By following these tips, financial professionals can significantly enhance the accuracy and effectiveness of their spot rate calculations from discount factors. These techniques will equip them to make informed decisions, manage risk, and navigate complex financial markets with confidence.

The concluding section of this article will explore advanced applications of spot rate calculations in various financial domains, demonstrating their practical significance and impact on financial decision-making.

Conclusion

In summary, calculating spot rates from discount factors is a fundamental financial technique that empowers professionals to accurately value future cash flows and make informed decisions in a variety of financial applications. This article has explored the intricacies of this calculation, providing a comprehensive guide to its formula, applications, and related concepts.

Key takeaways include the understanding that spot rates are influenced by prevailing interest rates, time to maturity, and risk factors. Furthermore, the formula for calculating spot rates from discount factors involves multiplying the future value of a cash flow by the corresponding discount factor. These insights underscore the importance of accurate data and robust estimation techniques in spot rate calculations.