Essential Guide to Calculating Daily Discount Rates

The daily discount rate, a vital financial concept, represents the rate at which future cash flows are discounted to determine their value as of today. It plays a crucial role in making informed investment decisions and financial planning. Historically, the development of the time value of money concept led to the use of discount rates to account for the opportunity cost of capital.

This comprehensive guide will delve into the different methods for calculating daily discount rates, empowering you to effectively evaluate investment opportunities and financial plans.

How to Calculate Daily Discount Rate

Calculating the daily discount rate accurately is essential for various financial applications. Key aspects to consider include:

- Time value of money

- Present value

- Future value

- Compounding

- Yield to maturity

- Risk-free rate

- Beta

- Expected return

- Inflation

- Taxation

These aspects are interconnected and influence the daily discount rate calculation. Understanding their interplay is crucial for accurate financial analysis and decision-making.

Time Value of Money

The time value of money (TVM) is a fundamental concept in finance that recognizes the difference between the value of money today and its value in the future due to its earning potential. In the context of calculating daily discount rates, TVM plays a pivotal role, as it allows us to compare the value of future cash flows to their present value.

- Present Value

PV is the current worth of a future sum of money, discounted at a specified interest rate. It helps determine the value of future cash flows today.

- Future Value

FV is the value of a present sum of money in the future, taking into account interest and compounding. It helps project the growth of investments over time.

- Compounding

Compounding refers to the interest earned on both the principal and the accumulated interest. It can significantly impact the growth of investments over time.

- Yield to Maturity

YTM is the annualized rate of return an investor expects to receive if they hold a debt security until its maturity date. It helps evaluate the potential return on fixed-income investments.

Understanding these facets of TVM is crucial for accurately calculating daily discount rates. By considering the time value of money, we can make informed decisions about investments, financial planning, and other economic activities that involve the flow of money over time.

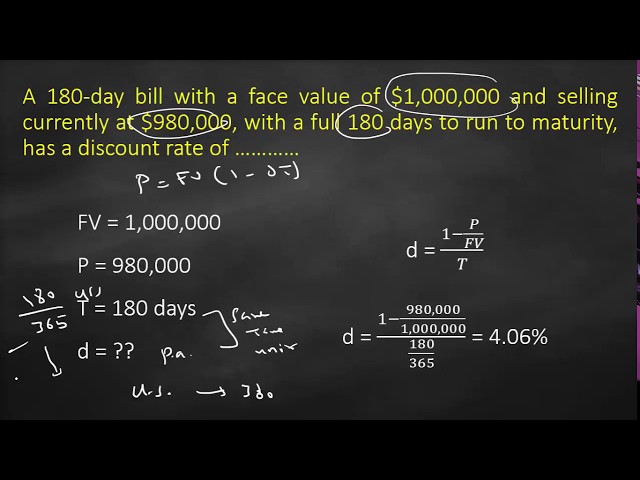

Present Value

Present value (PV) is a fundamental concept in finance that calculates the current worth of a future sum of money, discounted at a specified interest rate. It plays a pivotal role in determining the value of future cash flows today, making it a critical component of “how to calculate daily discount rate.” The daily discount rate represents the rate at which future cash flows are discounted to determine their present value. By understanding the relationship between present value and daily discount rate, we gain valuable insights into the time value of money and its impact on financial decision-making.

In the context of calculating daily discount rates, present value serves as the foundation for evaluating the worth of future cash flows. By discounting future cash flows back to the present using the daily discount rate, we can compare investments and make informed decisions about their potential returns. This concept is particularly important in capital budgeting, where businesses assess the profitability of long-term projects by calculating the present value of their expected cash flows.

Real-life examples of present value calculations are prevalent in various financial applications. For instance, when valuing a bond, investors calculate its present value to determine its fair price. Similarly, in project financing, the present value of future cash flows is used to assess the viability of a project and secure funding. Understanding the relationship between present value and daily discount rate empowers individuals and organizations to make sound financial decisions, mitigate risks, and optimize returns.

Future Value

Future value (FV) is a crucial element of calculating daily discount rates, as it represents the value of a present sum of money in the future, taking into account interest and compounding. By understanding the relationship between future value and daily discount rates, financial professionals and investors can make informed decisions about investments and financial planning.

In the context of calculating daily discount rates, future value serves as a key component for determining the present value of future cash flows. The daily discount rate, applied to future cash flows, effectively discounts them back to the present, allowing for comparison and evaluation of investments. Real-life examples of future value calculations include determining the maturity value of a bond or projecting the future worth of a retirement savings account, considering interest and compounding.

Understanding the relationship between future value and daily discount rates is critical for accurate financial analysis and decision-making. It enables the assessment of investment returns, comparison of alternative financing options, and planning for future financial goals. By considering the time value of money and the impact of interest rates, financial professionals and investors can make informed choices that maximize returns and mitigate risks.

Compounding

Compounding holds a pivotal role in calculating daily discount rates, reflecting the accumulation of interest on both the principal amount and the accumulated interest over time. This concept is fundamental for understanding the time value of money and making informed financial decisions.

- Exponential Growth

Compounding leads to exponential growth, where the value of an investment increases at an accelerating rate over time. This effect is particularly pronounced in long-term investments, highlighting the significance of time in financial planning.

- Impact on Present Value

Compounding directly affects the present value of future cash flows. A higher compounding rate results in a lower present value, emphasizing the importance of considering the time value of money when evaluating investments.

- Real-Life Examples

Compounding is evident in various financial instruments, such as savings accounts, bonds, and annuities. It allows individuals to grow their wealth over time, benefiting from the snowball effect of interest accumulation.

- Risk and Return

Compounding is intertwined with the relationship between risk and return. Higher-risk investments often offer higher compounding rates, potentially leading to greater returns over time. However, this also comes with increased volatility and the possibility of capital loss.

In conclusion, compounding is an indispensable aspect of calculating daily discount rates, influencing the present value of future cash flows and playing a crucial role in long-term financial planning. Understanding the impact of compounding empowers individuals and organizations to make informed investment decisions, assess risk-return profiles, and plan for financial success.

Yield to Maturity

Yield to maturity (YTM) is a critical component in calculating daily discount rates, influencing the present value of future cash flows and serving as a benchmark for fixed-income investments. Understanding its multifaceted nature is essential for accurate financial analysis and decision-making.

- Definition

YTM represents the annualized rate of return an investor expects to receive if they hold a debt security until its maturity date, considering all coupon payments and the final repayment of principal.

- Calculation

Calculating YTM involves solving for the discount rate that equates the present value of all future cash flows, including coupon payments and principal repayment, to the current market price of the bond.

- Real-Life Examples

YTM is widely used in the bond market to compare the potential returns of different bonds and to assess the overall health of the bond market.

- Impact on Discount Rates

YTM directly influences the calculation of daily discount rates, as it represents the rate at which future cash flows from a bond are discounted to determine their present value.

In conclusion, YTM is an indispensable concept in calculating daily discount rates, providing valuable insights into the present value of future cash flows and serving as a benchmark for fixed-income investments. Understanding its definition, calculation, and implications empowers individuals and organizations to make informed financial decisions and optimize returns from bond investments.

Risk-free rate

The risk-free rate is a fundamental concept in finance and serves as a critical component in calculating daily discount rates. Understanding the relationship between these two concepts is essential for accurate financial analysis and decision-making.

The daily discount rate is used to determine the present value of future cash flows, taking into account the time value of money and the associated risk. The risk-free rate represents the rate of return on an investment with no risk, typically approximated by the yield on government bonds. By incorporating the risk-free rate into the daily discount rate calculation, we can account for the opportunity cost of capital and the level of risk associated with the investment.

In practice, the risk-free rate is often used as a benchmark against which other investments are compared. Investments with higher risk are typically expected to offer a higher rate of return than the risk-free rate to compensate investors for taking on additional risk. Conversely, investments with lower risk may offer a return below the risk-free rate, reflecting their lower level of risk.

Understanding the connection between the risk-free rate and daily discount rate empowers financial professionals and investors to make informed decisions about investments, assess risk-adjusted returns, and optimize their financial strategies. By considering the time value of money, risk, and the opportunity cost of capital, they can make sound investment choices that align with their risk tolerance and financial goals.

Beta

Beta is a critical component in calculating daily discount rates, as it measures the systematic risk of an investment relative to the overall market. Understanding the relationship between beta and daily discount rates is essential for accurate financial analysis and decision-making.

The daily discount rate incorporates the risk-free rate and a risk premium that reflects the level of systematic risk associated with an investment. Beta serves as a quantitative measure of this risk premium, indicating the sensitivity of an investment’s returns to market movements. A higher beta indicates greater sensitivity to market fluctuations, resulting in a higher risk premium and, consequently, a higher daily discount rate.

Real-life examples of beta’s impact on daily discount rates can be observed in the pricing of stocks and bonds. Stocks with higher betas, such as those of small-cap companies or those operating in volatile industries, typically have higher daily discount rates due to their greater systematic risk. Conversely, bonds with lower betas, such as government bonds or those issued by large, stable companies, have lower daily discount rates due to their lower systematic risk.

Understanding the connection between beta and daily discount rates enables investors and financial professionals to make informed decisions about investments. By incorporating beta into the daily discount rate calculation, they can accurately assess the risk-adjusted returns of investments and make strategic decisions that align with their risk tolerance and financial goals.

Expected return

Expected return is a fundamental concept in finance that represents the average return an investor anticipates from an investment over a given period. It plays a pivotal role in calculating daily discount rates, as it serves as a key determinant of the risk premium. The risk premium, in turn, directly influences the daily discount rate, which is used to determine the present value of future cash flows.

As a critical component of daily discount rate calculation, expected return reflects the investor’s assessment of the potential return and risk associated with an investment. A higher expected return typically leads to a higher risk premium and, consequently, a higher daily discount rate. This is because investors demand a higher return for taking on greater risk. Conversely, a lower expected return generally results in a lower risk premium and a lower daily discount rate.

The relationship between expected return and daily discount rate has practical applications in various financial contexts. For instance, in capital budgeting, businesses use daily discount rates to assess the viability of long-term projects. By incorporating expected return into the calculation, they can evaluate projects based on their potential return and risk, making informed decisions about capital allocation.

Furthermore, understanding the connection between expected return and daily discount rate is crucial for investors seeking to optimize their portfolios. By considering the expected return and risk profile of different investments, investors can make strategic decisions that align with their financial goals and risk tolerance. This understanding empowers them to construct diversified portfolios that balance risk and return, aiming to maximize long-term wealth creation.

Inflation

Inflation is a persistent increase in the general price level of goods and services in an economy over time. It is a critical component in calculating daily discount rates because it affects the time value of money. When inflation is present, the value of money decreases over time, which means that future cash flows are worth less than current cash flows. This decrease in value must be taken into account when calculating daily discount rates, as it will impact the present value of future cash flows.

In practice, inflation is incorporated into the daily discount rate through the real risk-free rate. The real risk-free rate is the risk-free rate adjusted for inflation. It represents the rate of return that an investor can expect to receive on an investment with no risk, after taking into account the effects of inflation. The daily discount rate is then calculated using the real risk-free rate plus a risk premium that reflects the level of risk associated with the investment.

Understanding the relationship between inflation and daily discount rates is essential for accurate financial analysis and decision-making. By incorporating inflation into the daily discount rate calculation, investors and financial professionals can make informed decisions about investments, assess risk-adjusted returns, and optimize their financial strategies.

Taxation

Taxation plays a significant role in calculating daily discount rates due to its impact on the time value of money. Taxes reduce the future value of cash flows, as a portion of earnings must be paid to the government. This reduction in future value directly affects the present value of those cash flows, which is determined using the daily discount rate.

In practice, taxation is incorporated into the daily discount rate calculation through the after-tax cost of capital. The after-tax cost of capital represents the rate of return that an investor requires after considering the impact of taxes on their investment earnings. The daily discount rate is then calculated using the after-tax cost of capital plus a risk premium that reflects the level of risk associated with the investment.

Understanding the connection between taxation and daily discount rates is critical for accurate financial analysis and decision-making. By incorporating taxation into the daily discount rate calculation, businesses and investors can make informed decisions about investments, assess risk-adjusted returns, and optimize their financial strategies.

Frequently Asked Questions about Daily Discount Rate Calculation

This section addresses common questions and clarifies aspects of daily discount rate calculation, providing concise and informative answers.

Question 1: What is the purpose of calculating a daily discount rate?

Calculating the daily discount rate enables the determination of the present value of future cash flows, considering the time value of money and the level of risk associated with the investment.

Question 2: How does inflation impact the daily discount rate?

Inflation reduces the value of money over time, which must be accounted for in the daily discount rate calculation. The real risk-free rate, adjusted for inflation, is used to incorporate this effect.

Question 3: What is the relationship between beta and the daily discount rate?

Beta measures the systematic risk of an investment relative to the market. A higher beta typically leads to a higher risk premium and, consequently, a higher daily discount rate.

Question 4: How is taxation considered in the daily discount rate calculation?

Taxation reduces the future value of cash flows and is incorporated through the after-tax cost of capital. The daily discount rate uses this after-tax cost plus a risk premium.

Question 5: What is the significance of the risk-free rate in calculating the daily discount rate?

The risk-free rate represents the return on an investment with no risk. It serves as the foundation for the daily discount rate, with a risk premium added to account for the level of risk associated with the investment.

Question 6: How is the daily discount rate used in financial decision-making?

The daily discount rate is used in various financial applications, such as capital budgeting, project evaluation, and investment analysis. It enables informed decisions by considering the time value of money and the risk-return profile of investments.

These FAQs provide essential insights into the calculation and application of daily discount rates. Understanding these concepts is crucial for accurate financial analysis and decision-making.

In the following section, we will explore advanced techniques for calculating daily discount rates, enabling a deeper understanding and practical implementation of this critical financial concept.

Tips for Calculating Daily Discount Rates

This section provides practical tips to accurately calculate daily discount rates, ensuring informed financial decision-making.

Tip 1: Determine the appropriate time period.

The daily discount rate is calculated based on a specific time period. Ensure the period aligns with the investment horizon and cash flow timing.

Tip 2: Use reliable data sources.

Obtain accurate data for risk-free rates, inflation rates, and other relevant parameters from reputable sources.

Tip 3: Consider the risk profile of the investment.

Beta and other risk metrics should be used to determine the appropriate risk premium to add to the risk-free rate.

Tip 4: Account for inflation.

Use the real risk-free rate, which adjusts for inflation, to ensure the daily discount rate reflects the time value of money.

Tip 5: Incorporate tax implications.

Consider the after-tax cost of capital to account for the impact of taxes on cash flows.

Tip 6: Use a financial calculator or spreadsheet.

Simplify the calculation process by utilizing financial tools that automate the computations.

Tip 7: Review and adjust over time.

As market conditions and investment parameters change, periodically review and adjust the daily discount rate to maintain accuracy.

By following these tips, you can effectively calculate daily discount rates, enabling informed financial analysis and decision-making. These accurate calculations serve as a foundation for optimizing investments and achieving financial goals.

The concluding section of this article will delve into advanced applications of daily discount rates, showcasing their significance in complex financial modeling and decision-making processes.

Conclusion

This comprehensive guide has delved into the intricacies of calculating daily discount rates, emphasizing their significance in evaluating investments and making informed financial decisions. Key insights gained include the consideration of time value of money, risk-free rates, inflation, and taxation in the calculation process.

Understanding the interplay between these factors is crucial for accurate daily discount rate calculation. By incorporating risk premiums, adjusting for inflation, and considering tax implications, financial professionals and investors can determine the present value of future cash flows with greater precision. This knowledge empowers them to make strategic investment choices, optimize capital allocation, and achieve long-term financial goals.