How to Calculate Duration of Coupon Bond refers to the technique used to quantify the price sensitivity of a coupon bond to yield changes. It serves as a risk measure that helps bondholders understand how much the bond’s value will fluctuate based on interest rate movements. For instance, a bond with a duration of 5 years would lose approximately 5% of its value if interest rates were to increase by 1%.

Calculating bond duration is crucial for portfolio management, risk assessment, and making informed investment decisions. It enables investors to estimate the potential impact of interest rate shifts on their bond portfolio and can help them adjust their strategies accordingly. Historically, the concept of bond duration was first introduced in the 1960s by Frederick Macaulay. His influential work laid the foundation for our understanding of bond price dynamics.

This article will delve into the intricacies of calculating bond duration, exploring its components, formula, and practical applications. By providing a comprehensive guide, investors can enhance their proficiency in bond evaluation and make more effective financial decisions.

How to Calculate Duration of Coupon Bond

Understanding the essential aspects of bond duration calculation is crucial for accurate assessment of bond price sensitivity to interest rate fluctuations. Key aspects to consider include:

- Bond Price: Current market value of the bond.

- Coupon Rate: Fixed interest rate paid to bondholders.

- Maturity Date: Date when the bond principal is repaid.

- Yield to Maturity: Expected return on the bond held until maturity.

- Time to Maturity: Number of years until the bond matures.

- Present Value of Cash Flows: Value of future bond payments discounted to the present.

- Weighted Average Maturity: Average maturity of the bond’s cash flows.

- Modified Duration: Measure of price sensitivity to a small change in yield.

- Effective Duration: More accurate measure of price sensitivity for bonds with non-annual coupon payments.

- Key Rate Duration: Duration calculated at a specific interest rate.

These aspects provide a comprehensive framework for calculating bond duration, enabling investors to assess the potential impact of interest rate changes on their bond investments. Understanding the interconnections between these aspects and their relevance to the main topic of bond duration calculation is essential for informed decision-making in bond markets.

Bond Price

In the context of calculating bond duration, the bond price plays a pivotal role as it represents the present value of all future cash flows associated with the bond. It is a crucial factor that influences the bond’s duration and price sensitivity to interest rate changes.

- Face Value: The principal amount of the bond, which is repaid at maturity.

- Coupon Payments: Periodic interest payments made to bondholders throughout the life of the bond.

- Market Conditions: The prevailing economic and financial environment can affect the bond’s price, influencing its duration.

- Creditworthiness of the Issuer: The financial health and reputation of the bond issuer impact the bond’s price and, consequently, its duration.

These factors collectively determine the bond’s current market value, which serves as the basis for calculating its duration. A higher bond price typically corresponds to a longer duration, indicating greater price sensitivity to interest rate fluctuations. Conversely, a lower bond price generally results in a shorter duration, implying reduced price sensitivity.

Coupon Rate

The coupon rate, a crucial aspect of bond characteristics, plays a significant role in calculating bond duration. It represents the fixed interest rate paid to bondholders at regular intervals, typically semi-annually. Understanding the coupon rate’s nuances is essential for accurate duration calculation.

- Nominal Rate: The stated coupon rate printed on the bond certificate, expressed as a percentage of the face value.

- Annual Coupon Payment: The dollar value of interest paid to bondholders each year, calculated by multiplying the coupon rate by the face value.

- Frequency of Payments: Most bonds make semi-annual coupon payments; however, some bonds may have annual, quarterly, or even monthly payments.

- Impact on Duration: Bonds with higher coupon rates tend to have shorter durations, making them less sensitive to interest rate changes compared to bonds with lower coupon rates.

In summary, the coupon rate is a key determinant of bond duration. It influences the bond’s price sensitivity to interest rate fluctuations. Bonds with higher coupon rates generally have shorter durations, while those with lower coupon rates have longer durations. This understanding is fundamental for investors seeking to manage interest rate risk in their bond portfolios.

Maturity Date

In the context of bond duration calculation, the maturity date holds significant importance. It represents the point in time when the issuer redeems the bond and repays the principal amount to the bondholders. Understanding the nuances of the maturity date is crucial for accurate duration calculation and risk assessment.

- Final Payment Date: The maturity date marks the end of the bond’s life, when investors receive the remaining principal balance.

- Impact on Duration: Bonds with longer maturities tend to have longer durations, making them more sensitive to interest rate changes. Conversely, bonds with shorter maturities have shorter durations and are less sensitive to interest rate fluctuations.

- Influence on Yield-to-Maturity: The maturity date is a key factor in determining the bond’s yield-to-maturity (YTM), which is the annualized rate of return an investor can expect to earn by holding the bond until maturity.

- Callable Bonds: Some bonds may have a call feature, which gives the issuer the option to redeem the bond before maturity. Callable bonds typically have shorter effective durations compared to non-callable bonds.

In summary, the maturity date plays a pivotal role in determining bond duration and is a crucial factor for investors to consider when evaluating the potential price sensitivity and return profile of a bond.

Yield to Maturity

Yield to maturity (YTM) plays a crucial role in determining the duration of a coupon bond. It represents the annualized rate of return an investor can expect to earn by holding the bond until maturity, assuming all coupon payments and the principal are paid as scheduled. Understanding YTM is essential for accurate duration calculation and risk assessment.

- Coupon Payments: YTM considers the present value of all future coupon payments received by the investor over the bond’s life.

- Face Value: YTM also incorporates the present value of the bond’s face value, which is repaid at maturity.

- Time to Maturity: The length of time until the bond matures impacts the YTM calculation, with longer maturities generally resulting in higher YTM.

- Market Price: The current market price of the bond influences the YTM, as it reflects the present value of all future cash flows based on prevailing market conditions.

In summary, YTM is a critical component of duration calculation, as it captures the expected total return an investor can earn by holding the bond until maturity. Bonds with higher YTMs tend to have longer durations, indicating greater price sensitivity to interest rate changes.

Time to Maturity

In the context of “how to calculate duration of coupon bond”, “Time to Maturity” holds great significance. It represents the number of years until the bond’s maturity date, when the issuer repays the bond’s face value to the bondholder. Understanding the nuances of “Time to Maturity” is paramount for accurate duration calculation and effective bond portfolio management.

- Years-to-Maturity: This refers to the actual number of years remaining until the bond matures. It directly influences the bond’s duration, with longer maturities typically resulting in longer durations.

- Weighted Average Life: For bonds with varying cash flow streams, such as callable or putable bonds, “Time to Maturity” is calculated as the weighted average of the time until each cash flow is received.

- Market Conventions: In practice, “Time to Maturity” is often calculated using market conventions, such as the “Rule of 78” or the “30/360” convention, which provide standardized methods for calculating bond duration.

- Impact on Duration: “Time to Maturity” is inversely related to duration. Bonds with longer maturities have longer durations and are more sensitive to interest rate changes. Conversely, bonds with shorter maturities have shorter durations and are less sensitive to interest rate fluctuations.

By comprehending the various facets of “Time to Maturity”, investors can gain a deeper understanding of how it impacts bond duration. This knowledge is crucial for making informed investment decisions, managing interest rate risk, and optimizing bond portfolio performance.

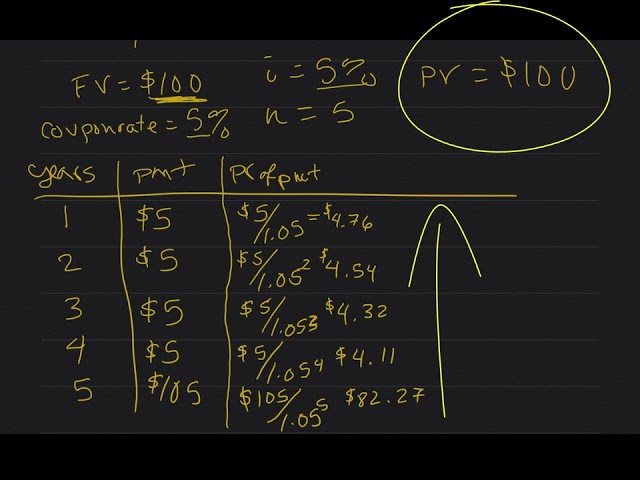

Present Value of Cash Flows

In the context of “how to calculate duration of coupon bond,” the Present Value of Cash Flows holds immense significance. It represents the value of all future cash flows from a bond, discounted to the present using an appropriate discount rate. Understanding this concept is crucial for accurate duration calculation.

- Coupon Payments: These are the periodic interest payments made to bondholders throughout the bond’s life. The present value of these payments is a major component of the bond’s overall value.

- Face Value: This is the principal amount of the bond, which is repaid at maturity. Its present value forms a significant portion of a bond’s present value, especially for bonds with longer maturities.

- Discount Rate: The discount rate used in the calculation is typically the bond’s yield to maturity (YTM). It represents the required rate of return for holding the bond until maturity and directly influences the present value of the cash flows.

- Time Value of Money: The time value of money implies that a dollar today is worth more than a dollar in the future due to inflation and the potential for earning interest. Discounting future cash flows to the present reflects this concept.

By considering the present value of future cash flows, investors can determine the fair value of a bond and assess its sensitivity to changes in interest rates. This knowledge enables informed investment decisions and effective management of bond portfolios.

Weighted Average Maturity

Within the context of “how to calculate duration of coupon bond,” “Weighted Average Maturity” emerges as a crucial concept. It represents the average maturity of all the bond’s cash flows, taking into account each payment’s size and timing. This weighted average provides insights into the bond’s overall sensitivity to interest rate fluctuations.

- Time until Receipt: Each cash flow’s maturity is measured as the time until it is received, considering both coupon payments and the repayment of principal at maturity.

- Cash Flow Size: The size of each cash flow, including both coupon payments and the face value, influences its weight in the calculation.

- Discounting: The time value of money is considered by discounting each cash flow back to the present using an appropriate discount rate, typically the bond’s yield to maturity.

- Weighted Sum: The weighted average maturity is calculated as the weighted sum of the discounted cash flows, with each cash flow weighted by its present value.

Understanding “Weighted Average Maturity” is essential for bond investors as it provides a more accurate measure of a bond’s maturity profile compared to simply using the stated maturity date. Bonds with longer weighted average maturities are more sensitive to interest rate changes, while shorter weighted average maturities indicate less sensitivity. This knowledge enables investors to make informed decisions about their bond investments and manage interest rate risk effectively.

Modified Duration

Within the context of “how to calculate duration of coupon bond,” “Modified Duration” holds critical importance. It quantifies the price sensitivity of a bond to a small change in yield, providing valuable insights into how bond prices fluctuate in response to interest rate movements. Modified Duration is a crucial component of duration calculation, as it captures the bond’s price elasticity with respect to yield changes.

In essence, a bond’s Modified Duration measures the percentage change in its price for a given change in yield. This relationship is inversely proportional, meaning that as yield increases, bond prices tend to decrease, and vice versa. The Modified Duration provides a more accurate assessment of price sensitivity compared to Traditional Duration, particularly for bonds with non-annual coupon payments or complex cash flow structures.

Real-life examples further illustrate the significance of Modified Duration. Consider two bonds with the same Traditional Duration but different coupon structures. A bond with semi-annual coupon payments will have a shorter Modified Duration than a bond with annual coupon payments, indicating that the semi-annual bond’s price will be less sensitive to yield changes. This is because the more frequent coupon payments provide a cushion against price fluctuations.

Understanding Modified Duration empowers investors with valuable insights for making informed bond investment decisions. It enables them to assess the potential impact of interest rate changes on their bond portfolios and adjust their strategies accordingly. Moreover, it facilitates comparisons between bonds with varying characteristics, allowing investors to select those that best align with their risk tolerance and investment objectives.

Effective Duration

In the realm of “how to calculate duration of coupon bond,” “Effective Duration” emerges as a refined metric that tackles the limitations of traditional duration measures, providing a more accurate gauge of price sensitivity for bonds with non-annual coupon payments. This enhanced precision stems from its consideration of the timing and frequency of coupon payments, capturing nuances that traditional duration overlooks.

- Continuous Compounding: Effective Duration incorporates continuous compounding of interest payments, reflecting the actual yield accrual process, unlike traditional duration which assumes discrete compounding.

- Non-Annual Coupon Payments: Effective Duration accounts for bonds with coupon payments made at intervals other than annually, such as semi-annually or quarterly, providing a more granular measure of price sensitivity.

- Complex Cash Flows: Effective Duration can handle complex cash flow structures, such as bonds with embedded options or callable features, which can distort traditional duration calculations.

- Real-World Accuracy: Effective Duration aligns more closely with the actual price behavior of bonds in response to yield changes, making it a more reliable tool for risk assessment and portfolio management.

In conclusion, Effective Duration stands as a superior measure of price sensitivity for bonds with non-annual coupon payments, addressing the shortcomings of traditional duration calculations. By incorporating continuous compounding, accommodating various coupon payment frequencies, handling complex cash flows, and aligning with real-world price behavior, Effective Duration empowers investors with a more precise understanding of bond price dynamics and enables more informed investment decisions.

Key Rate Duration

The concept of “Key Rate Duration” holds significant relevance within the broader context of “how to calculate duration of coupon bond.” It represents the duration of a bond calculated at a specific interest rate, providing valuable insights into the bond’s price sensitivity at that particular yield level. Understanding the relationship between Key Rate Duration and bond duration is crucial for effective bond portfolio management and risk assessment.

Key Rate Duration becomes a critical component of bond duration calculation when assessing the bond’s price behavior under specific interest rate scenarios. It allows investors to gauge the potential impact of interest rate changes on the bond’s value at a given yield level. By analyzing the Key Rate Duration at different interest rates, investors can develop a more nuanced understanding of the bond’s price sensitivity across a range of market conditions.

In practice, Key Rate Duration finds applications in various areas. For instance, in duration matching strategies, it helps investors align the duration of their bond portfolio with their investment horizon and risk tolerance. Moreover, it assists in constructing bond portfolios with targeted interest rate sensitivities, enabling investors to manage interest rate risk more effectively.

In summary, Key Rate Duration provides a valuable tool for bond investors to evaluate the price sensitivity of a bond at specific interest rates. By incorporating Key Rate Duration into bond duration calculations, investors gain a more comprehensive understanding of how their bond portfolio might perform under different yield scenarios, empowering them to make more informed investment decisions.

Frequently Asked Questions about Calculating Duration of Coupon Bond

This section addresses common questions and clarifies concepts related to calculating bond duration, providing essential insights for a comprehensive understanding of the topic.

Question 1: What is the significance of bond duration?

Bond duration quantifies the price sensitivity of a bond to interest rate changes, aiding investors in understanding how their bond investments will respond to fluctuations in the yield curve.

Question 2: How is bond duration calculated using the Macaulay Duration formula?

The Macaulay Duration formula calculates bond duration by summing the present value of each cash flow, multiplied by its time to maturity, and dividing the result by the bond’s current price.

Question 3: What are the key factors influencing bond duration?

Bond duration is primarily influenced by factors such as coupon rate, yield-to-maturity, time to maturity, and the present value of cash flows.

Question 4: How does bond duration differ from modified duration?

Modified duration is a refinement of traditional duration that considers the non-linear relationship between bond price and yield. It provides a more accurate measure of price sensitivity, particularly for bonds with non-annual coupon payments.

Question 5: What is the relevance of effective duration in bond valuation?

Effective duration incorporates continuous compounding and considers complex cash flow structures, enhancing the accuracy of bond valuation and risk assessment.

Question 6: How can investors use duration analysis in portfolio management?

Duration analysis helps investors align the interest rate sensitivity of their bond portfolio with their investment objectives and risk tolerance, enabling more effective portfolio management.

These FAQs provide foundational knowledge for understanding bond duration and its implications. The following section will delve into advanced topics and practical applications of duration analysis in bond investing.

Tips for Calculating Duration of Coupon Bond

To enhance your understanding and application of bond duration, consider these actionable tips:

Tip 1: Grasp the Relationship Between Duration and Price Sensitivity: Understand that bond duration quantifies how much a bond’s price changes in response to interest rate fluctuations.

Tip 2: Utilize the Macaulay Duration Formula: Calculate bond duration using the Macaulay Duration formula, which considers the present value of each cash flow and its time to maturity.

Tip 3: Consider Modified Duration for Accurate Assessment: Employ modified duration to capture the non-linear relationship between bond price and yield, providing a more precise measure of price sensitivity.

Tip 4: Analyze Effective Duration for Non-Annual Coupons: Use effective duration to account for continuous compounding and complex cash flow structures, enhancing valuation accuracy.

Tip 5: Examine Key Rate Duration for Specific Interest Rates: Calculate duration at specific interest rates using key rate duration to evaluate price sensitivity under different yield scenarios.

Tip 6: Integrate Duration Analysis into Portfolio Management: Align your bond portfolio’s duration with your investment horizon and risk tolerance through duration analysis.

Tip 7: Utilize Duration to Compare Bonds: Compare the durations of different bonds to assess their relative price sensitivity and make informed investment decisions.

Tip 8: Stay Updated on Duration Calculations: Familiarize yourself with the latest advancements and techniques in duration calculation to ensure accurate assessments.

In summary, applying these tips can significantly enhance your ability to calculate and interpret bond duration, enabling you to make well-informed bond investment decisions.

Moving forward, the concluding section of this article will summarize the key takeaways and emphasize the importance of accurate duration calculations for successful bond investing.

Conclusion

Understanding how to calculate duration of coupon bond is an indispensable skill for bond investors and portfolio managers. It empowers informed decision-making by quantifying the price sensitivity of a bond to interest rate changes. Key points to remember include:

- Bond duration measures the extent to which a bond’s price fluctuates in response to yield movements.

- Modified and effective duration provide more accurate assessments for bonds with non-annual coupon payments and complex cash flows, respectively.

- Duration analysis enables investors to align their bond portfolio with their risk tolerance and investment horizon, ensuring optimal returns and risk management.

Accurate duration calculations are crucial for successful bond investing, enabling investors to navigate interest rate fluctuations and make well-informed investment decisions. By embracing these concepts and incorporating them into your investment strategy, you can unlock the full potential of bond duration as a valuable tool for bond portfolio management and wealth accumulation.