Calculating a coupon payment is a crucial step in understanding fixed-income securities and financial markets. A coupon payment represents the periodic interest a bondholder by the issuer of a bond.

Coupon payments are essential for investors because they provide a regular, predictable source of income. Historically, the development of coupon bonds in the 18th century revolutionized government financing, enabling significant infrastructure projects and economic growth.

This article explores the key details and formula for calculating a coupon payment, providing practical insights for investors and financial professionals alike.

How to Calculate a Coupon Payment

Calculating a coupon payment is essential for evaluating fixed-income investments and cashflows. It involves several key aspects:

- Face value

- Coupon rate

- Payment frequency

- Time to maturity

- Accrual period

- Payment date

- Missed payments

- Callable bonds

Understanding these aspects allows investors to accurately determine the periodic interest payments they will receive from a bond, assess the bond’s value, and make informed investment decisions. It is also crucial for issuers to calculate coupon payments correctly to meet their debt obligations and maintain investor confidence.

Face Value

The face value, also known as “par value” or “principal,” is the nominal value of a bond, representing the amount that the issuer promises to repay to the bondholder at maturity. It serves as the basis for calculating coupon payments and is a crucial aspect of determining the bond’s overall value.

- Nominal Amount: The face value represents the amount borrowed by the issuer from the bondholder.

- Repayment Amount: At maturity, the bondholder is entitled to receive the face value, which is the principal amount of the loan.

- Coupon Calculation Base: Coupon payments are typically calculated as a percentage of the face value.

- Bond Value Impact: The face value influences the bond’s price and yield, as investors consider it along with other factors.

Understanding the face value is essential for investors to assess the potential return on their investment and for issuers to determine the cost of borrowing. It provides a benchmark against which to compare different bonds and make informed decisions.

Coupon rate

The coupon rate is a crucial factor in determining coupon payments. It represents the annual interest rate that the bond issuer promises to pay to bondholders. Understanding the various facets of the coupon rate is essential for accurately calculating coupon payments and assessing the overall value of a bond.

- Nominal Rate: The stated annual interest rate specified on the bond certificate, expressed as a percentage of the face value.

- Effective Rate: The actual annual yield or return on the bond, taking into account the bond’s price and the frequency of coupon payments.

- Zero-Coupon Rate: A special case where the bond is issued at a deep discount and does not pay periodic coupons, resulting in a higher return at maturity.

- Floating Rate: A variable interest rate that adjusts periodically based on a reference rate, such as LIBOR, providing protection against interest rate fluctuations.

Understanding these different aspects of the coupon rate empowers investors to make informed decisions when evaluating and comparing bonds. It also enables issuers to structure bonds that meet their financing needs and align with investors’ risk tolerance and return expectations.

Payment frequency

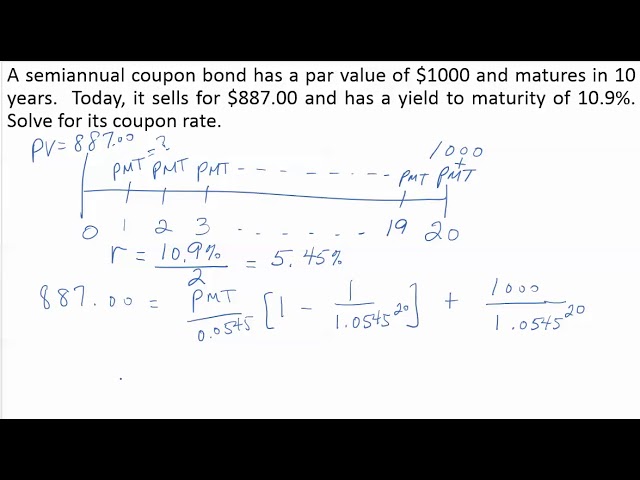

Payment frequency is a critical component of calculating coupon payments. It determines how often the bondholder receives interest payments and directly affects the calculation formula. Bonds typically have annual, semi-annual, quarterly, or monthly payment frequencies.

The payment frequency impacts the effective annual yield of the bond. For example, a bond with a 5% annual coupon rate paid semi-annually has an effective annual yield of 5.06%, slightly higher than the nominal rate due to the more frequent compounding. Understanding the relationship between payment frequency and effective yield is essential for investors to compare bonds accurately.

In practice, payment frequency can also influence bond prices. Bonds with more frequent payment schedules tend to be more attractive to investors, especially those seeking regular income streams. As a result, these bonds may trade at a premium compared to bonds with less frequent payments but similar overall yields.

Overall, payment frequency is an essential consideration for both investors and issuers. It affects the calculation of coupon payments, effective yield, and bond valuation. Understanding this relationship empowers investors to make informed decisions and issuers to structure bonds that meet their financing needs and align with investor preferences.

Time to maturity

Time to maturity is a critical factor in calculating coupon payments as it determines the duration of the bond and the number of coupon payments an investor will receive. It is the period from the issuance date of a bond to its maturity date, when the principal is repaid to the bondholder.

- Length of Bond: Time to maturity defines the life of a bond, influencing its risk and return profile.

- Coupon Payment Frequency: The number of coupon payments received by an investor is directly related to the time to maturity and payment frequency.

- Present Value: Time to maturity plays a crucial role in determining the present value of a bond, as it affects the discounting of future cash flows.

- Interest Rate Risk: Bonds with longer time to maturity are more sensitive to interest rate changes, making their prices more volatile.

In summary, time to maturity is a fundamental element in calculating coupon payments and understanding the overall characteristics of a bond. It influences the number of payments, the present value, and the risk associated with the investment. Therefore, it is crucial for investors to consider time to maturity when evaluating and comparing different bonds.

Accrual period

Within the realm of calculating coupon payments, the accrual period holds significance as the time frame over which interest accrues on a bond but is not yet payable to the bondholder. Understanding its various aspects is essential for accurate calculation and interpretation of coupon payments.

- Payment Dates: Accrual periods are typically defined by the payment dates of a bond, establishing clear intervals for interest accumulation.

- Maturity Date: The accrual period also considers the maturity date, which marks the end of the bond’s life and the final coupon payment.

- Settlement Date: When a bond is purchased or sold, the accrual period will be adjusted to account for the settlement date, ensuring that accrued interest is appropriately credited or debited.

- Missed Payments: In cases where a bond issuer misses a scheduled coupon payment, the accrual period will continue to accumulate interest, and the bondholder will eventually receive the overdue payment plus any accrued interest.

By understanding the nuances of the accrual period, investors can accurately calculate coupon payments, anticipate future cash flows, and make informed decisions about bond investments. It provides a framework for tracking interest accumulation and ensuring that bondholders receive fair compensation for their investment.

Payment date

In the context of calculating coupon payments, the payment date holds critical importance, as it directly affects the calculation process and the timing of interest payments to bondholders. The payment date is the predetermined date on which the bond issuer is obligated to make the scheduled coupon payment to bondholders. Understanding the connection between payment date and coupon payment calculation is essential for accurate financial planning and investment decision-making.

The payment date is a fundamental component of coupon payment calculation because it determines the accrual period, which is the time frame over which interest accumulates on the bond. The accrual period begins on the day after the previous coupon payment date and ends on the payment date. The length of the accrual period can vary depending on the bond’s specific terms, but it typically aligns with the payment frequency, such as semi-annually or quarterly.

To illustrate, let’s consider a bond with a face value of $1,000 and a 6% annual coupon rate, paid semi-annually. If the payment dates are June 15th and December 15th, the accrual period for the June 15th payment begins on December 16th and ends on June 15th. During this period, interest accrues on the bond, and the bondholder earns interest income. The coupon payment on June 15th is calculated as the product of the face value, the coupon rate, and the fraction of the year represented by the accrual period (182 days / 365 days = 0.5). Therefore, the coupon payment on June 15th would be $1,000 0.06 0.5 = $30.

Understanding the payment date and its relationship with coupon payment calculation empowers investors and financial professionals to accurately determine the timing and amount of interest payments they will receive or pay. It also helps them make informed decisions about bond purchases and sales, ensuring that they receive fair compensation for their investment.

Missed payments

Missed payments are a crucial consideration in calculating coupon payments as they can impact the overall return and risk profile of a bond investment. Understanding the various aspects of missed payments is essential for investors to make informed decisions.

- Default: Default occurs when the bond issuer fails to make a scheduled coupon payment. This can have severe consequences for bondholders, including loss of income and potential principal impairment.

- Grace period: Many bonds have a grace period, which provides the issuer with a short window of time to make a missed payment before being considered in default. During this period, bondholders may still receive interest payments, but the bond’s value may decline due to increased risk.

- Partial payment: In some cases, the issuer may make a partial payment, covering only a portion of the scheduled coupon payment. Bondholders will receive the partial payment, and the remaining amount will accrue as unpaid interest.

- Bankruptcy: If the bond issuer declares bankruptcy, missed payments may become permanent. Bondholders may lose their entire investment or receive only a portion of their principal and accrued interest through the bankruptcy process.

Understanding these aspects of missed payments empowers investors to assess the creditworthiness of bond issuers, anticipate potential risks, and make informed decisions about their bond investments. It helps them calculate coupon payments accurately, considering the possibility of missed payments and their impact on the bond’s value and return.

Callable bonds

Callable bonds introduce an additional layer of complexity to the calculation of coupon payments. A callable bond is a debt security that grants the issuer the option to repurchase the bond at a specified price before its maturity date. This feature can have a significant impact on the calculation of coupon payments, as it introduces the possibility of early repayment.

When a callable bond is issued, the issuer typically sets a call price, which is the price at which the bond can be repurchased. If interest rates decline after the bond is issued, the issuer may choose to call the bond and refinance at a lower rate, resulting in the termination of coupon payments to the bondholders. Conversely, if interest rates rise, the issuer is less likely to call the bond, as it would have to pay a premium to do so.

For investors, the callability feature adds an element of uncertainty to the calculation of coupon payments. While the coupon rate is fixed at the time of issuance, the actual number of coupon payments received may be reduced if the bond is called early. This can impact the overall yield and return on the investment.

To account for the callability feature, investors need to consider the potential impact of early repayment when calculating coupon payments. This can be done by using a modified duration calculation, which incorporates the probability of the bond being called and the expected call date. By understanding the relationship between callable bonds and coupon payment calculation, investors can make more informed investment decisions and accurately assess the risks and rewards associated with these bonds.

Frequently Asked Questions (FAQs) on Calculating Coupon Payments

This section provides answers to common questions and addresses potential areas of confusion regarding coupon payment calculations.

Question 1: What factors determine coupon payments?

Coupon payments are determined by the face value of the bond, the annual coupon rate, and the number of payment periods per year.

Question 2: How does the payment frequency affect the coupon amount?

More frequent payment schedules result in smaller individual coupon payments, but the total annual interest payment remains unchanged.

Question 3: What happens if I buy a bond between coupon payment dates?

You will receive a prorated payment to cover the accrued interest from the previous payment date to the date of purchase.

Question 4: Can coupon payments change over time?

In the case of floating-rate bonds, coupon payments adjust periodically based on a reference rate, such as LIBOR.

Question 5: What is the relationship between callable bonds and coupon payments?

Callable bonds give the issuer the option to repurchase the bond before maturity, potentially affecting the number of coupon payments received.

Question 6: How can I calculate the total interest earned from a bond?

Multiply the coupon rate by the face value to determine the annual interest payment, then multiply by the number of years until maturity.

These FAQs provide a concise overview of key considerations for calculating coupon payments, empowering investors to make informed decisions.

The next section will delve deeper into advanced topics related to coupon payment calculations and strategies, such as present value analysis and yield calculations.

Tips for Calculating Coupon Payments Accurately

This section provides practical tips to assist in the precise calculation of coupon payments, ensuring accurate financial planning and informed investment decisions.

Tip 1: Determine the Bond’s Face Value and Coupon Rate: Identify the face value, which represents the principal amount borrowed, and the annual coupon rate, which determines the interest payments.

Tip 2: Establish the Payment Frequency: Confirm the frequency of coupon payments, whether annually, semi-annually, quarterly, or monthly, as this impacts the calculation intervals.

Tip 3: Calculate the Accrued Interest: Determine the accrued interest, which represents the interest earned since the last payment date, to ensure proper accounting.

Tip 4: Consider Missed Payments: In case of missed payments, calculate the unpaid interest and adjust the payment schedule accordingly.

Tip 5: Factor in Callable Bonds: If the bond is callable, assess the potential impact of early repayment on the coupon payment calculations.

Tip 6: Utilize Financial Calculators or Spreadsheets: Leverage financial calculators or spreadsheets to simplify and expedite the coupon payment calculation process.

Following these tips empowers investors and financial professionals to calculate coupon payments accurately, enabling informed decision-making and effective bond investment strategies.

The concluding section will explore advanced concepts related to coupon payment calculations, providing a comprehensive understanding of this critical aspect of fixed-income investments.

Conclusion

This article has explored the intricacies of calculating coupon payments, providing insights into the factors and considerations involved in this crucial aspect of fixed-income investments. Key takeaways include the significance of understanding the face value, coupon rate, payment frequency, and time to maturity in determining coupon payments. Additionally, the article highlighted the impact of missed payments and callable bonds on the calculation process.

Calculating coupon payments accurately is essential for investors to assess the potential return on their investment and make informed decisions. It also enables issuers to structure bonds that meet their financing needs while aligning with investor expectations. By understanding the concepts outlined in this article, individuals can confidently navigate the complexities of coupon payment calculations and enhance their fixed-income investment strategies.