Finding net income in QuickBooks involves understanding the specific accounting procedures within the software.

Determining net income is crucial for businesses as it represents their financial performance and profitability. By tracking income and expenses, businesses can identify areas for improvement and make informed decisions. QuickBooks, a leading accounting software, provides tools to calculate net income efficiently.

This article will guide you through the steps to find net income in QuickBooks, highlighting important features and considerations along the way.

How to Find Net Income in QuickBooks

Understanding how to find net income in QuickBooks is vital for businesses to manage their finances effectively.

- Business Transactions

- Income Tracking

- Expense Classification

- Profit and Loss Statement

- Depreciation and Amortization

- Inventory Management

- Tax Calculations

- Financial Reporting

- Industry-Specific Features

- Software Updates

These aspects are interconnected and provide a comprehensive understanding of how to find net income in QuickBooks. By considering each aspect thoroughly, businesses can accurately determine their financial performance and make informed decisions.

Business Transactions

Every business transaction, whether a sale, purchase, or expense, impacts the calculation of net income in QuickBooks. These transactions are recorded in the company’s accounting system, providing a detailed history of all financial activities. By understanding the types of business transactions and how they are classified in QuickBooks, users can accurately track income and expenses, which is essential for determining net income.

For example, when a product is sold, QuickBooks records the transaction as an increase in sales revenue. Similarly, when a purchase is made, QuickBooks records the expense associated with that purchase. By tracking these transactions, businesses can create reports that summarize their income and expenses over a specific period of time, such as a month or quarter. These reports are essential for calculating net income, which is the difference between total income and total expenses.

Without a clear understanding of business transactions and how they are recorded in QuickBooks, it is difficult to find net income accurately. By mastering this aspect, businesses can gain valuable insights into their financial performance and make informed decisions to improve profitability.

Income Tracking

Income tracking is a critical component of how to find net income in QuickBooks. It involves recording all sources of income, including sales revenue, interest income, and dividend income. Accurate income tracking is essential for several reasons. First, it ensures that all income is accounted for, which is necessary for calculating net income correctly. Second, it provides a detailed history of income, which can be used to identify trends and patterns. This information can be valuable for making informed decisions about the business, such as how to increase sales or reduce expenses.

There are several ways to track income in QuickBooks. One common method is to use the Sales Receipts feature. This feature allows businesses to create and track invoices for sales of goods or services. QuickBooks also allows businesses to track income from other sources, such as interest and dividends. By using the appropriate features and tools, businesses can ensure that all income is recorded accurately.

Income tracking is essential for any business that wants to find net income in QuickBooks. By accurately tracking income, businesses can gain valuable insights into their financial performance and make informed decisions about the future.

Expense Classification

Expense classification is a critical aspect of how to find net income in QuickBooks. It involves categorizing expenses into different types, such as cost of goods sold, operating expenses, and other expenses. Accurate expense classification is essential for several reasons. First, it ensures that expenses are allocated to the correct accounts, which is necessary for calculating net income correctly. Second, it provides a detailed history of expenses, which can be used to identify trends and patterns. This information can be valuable for making informed decisions about the business, such as how to reduce expenses or increase profits.

- Fixed Expenses: These expenses remain relatively constant from month to month, regardless of the level of activity. Examples include rent, insurance, and salaries.

- Variable Expenses: These expenses vary with the level of activity. Examples include cost of goods sold, shipping costs, and commissions.

- Direct Expenses: These expenses can be directly traced to a specific product or service. Examples include raw materials, direct labor, and freight-in.

- Indirect Expenses: These expenses cannot be directly traced to a specific product or service. Examples include administrative expenses, marketing expenses, and utilities.

By understanding the different types of expenses and how to classify them, businesses can accurately calculate net income in QuickBooks. This information can then be used to make informed decisions about the business, such as how to reduce expenses or increase profits.

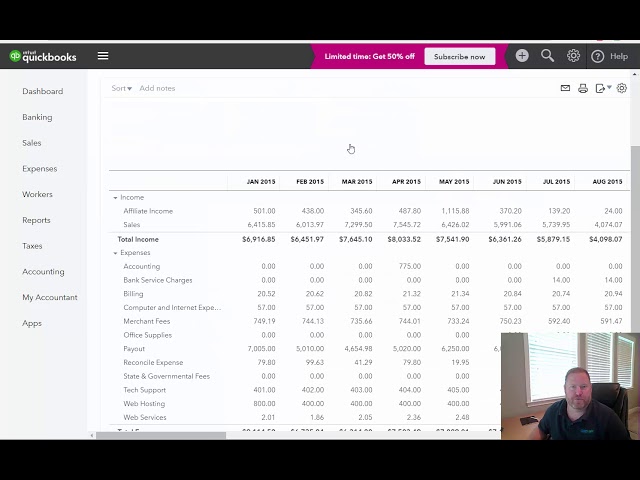

Profit and Loss Statement

The profit and loss statement, also known as the income statement, is a financial statement that summarizes the revenues, expenses, and profits of a business over a specific period of time. It is an essential tool for understanding the financial performance of a business and is used to calculate net income.

- Revenue: Revenue is the income generated from the sale of goods or services. It is the first line item on the profit and loss statement and is the starting point for calculating net income.

- Expenses: Expenses are the costs incurred in the process of generating revenue. They can be divided into two categories: operating expenses and non-operating expenses. Operating expenses are the costs associated with the day-to-day operations of the business, such as salaries, rent, and utilities. Non-operating expenses are costs that are not related to the core operations of the business, such as interest expense and foreign exchange losses.

- Net Income: Net income is the difference between revenue and expenses. It is the profit or loss generated by the business over a specific period of time and is the bottom line of the profit and loss statement.

The profit and loss statement is an important tool for businesses of all sizes. It provides a snapshot of the financial performance of the business and can be used to identify trends, make comparisons, and make informed decisions about the future.

Depreciation and Amortization

Depreciation and amortization are accounting methods used to allocate the cost of long-term assets over their useful lives. Depreciation is used for tangible assets, such as property, plant, and equipment, while amortization is used for intangible assets, such as patents, trademarks, and copyrights. Both depreciation and amortization reduce the value of the asset on the balance sheet and create an expense on the income statement. This expense reduces net income, which is the profit a company makes after subtracting all of its expenses from its revenue.

Depreciation and amortization are critical components of how to find net income in QuickBooks because they ensure that the cost of long-term assets is spread out over their useful lives. This prevents companies from overstating their net income in the early years of an asset’s life and understating it in the later years. By allocating the cost of the asset evenly over its useful life, depreciation and amortization provide a more accurate picture of a company’s profitability.

For example, if a company purchases a new piece of equipment for $10,000 and expects it to last for five years, it will depreciate the equipment by $2,000 per year. This means that the company will record an expense of $2,000 on its income statement each year for five years. This expense will reduce the company’s net income by $2,000 each year.

Understanding depreciation and amortization is essential for finding net income in QuickBooks. By correctly depreciating and amortizing long-term assets, companies can ensure that their financial statements are accurate and that they are paying the correct amount of taxes.

Inventory Management

Inventory management plays a critical role in how to find net income in QuickBooks. By accurately tracking inventory levels and costs, businesses can ensure that their financial statements are accurate and that they are paying the correct amount of taxes.

- Inventory Valuation: Businesses must choose an inventory valuation method, such as FIFO, LIFO, or weighted average, to determine the cost of goods sold. The choice of method can have a significant impact on net income.

- Inventory Tracking: Businesses must track inventory levels to prevent overstocking or understocking. Accurate inventory tracking can help businesses optimize their inventory levels and reduce costs.

- Cost of Goods Sold: The cost of goods sold is a key expense that reduces net income. Businesses must accurately calculate the cost of goods sold to ensure that their financial statements are accurate.

- Inventory Turnover: Inventory turnover measures how quickly a business is selling its inventory. A high inventory turnover ratio indicates that a business is efficiently managing its inventory and generating revenue.

By understanding inventory management and its impact on net income, businesses can use QuickBooks to accurately track their inventory and make informed decisions about their inventory levels and costs.

Tax Calculations

Tax calculations are an essential aspect of how to find net income in QuickBooks. By accurately calculating taxes, businesses can ensure that they are paying the correct amount of taxes and that their financial statements are accurate.

- Tax Rates: Businesses must be aware of the various tax rates that apply to their business, such as federal income tax, state income tax, and sales tax. The correct tax rate must be applied to each transaction to ensure accurate tax calculations.

- Tax Deductions: Businesses may be eligible for various tax deductions, such as the home office deduction, the charitable contribution deduction, and the research and development deduction. Taking advantage of all allowable tax deductions can reduce net income and tax liability.

- Tax Credits: Businesses may also be eligible for tax credits, such as the child tax credit and the earned income tax credit. Tax credits directly reduce tax liability, which can increase net income.

- Estimated Taxes: Businesses are required to make estimated tax payments throughout the year to the IRS. These payments are based on the estimated tax liability for the year. By making estimated tax payments, businesses can avoid penalties for underpaying taxes.

Understanding tax calculations is essential for finding net income in QuickBooks. By correctly calculating taxes, businesses can ensure that they are paying the correct amount of taxes and that their financial statements are accurate. This can help businesses avoid penalties and interest charges, and can also help them plan for the future.

Financial Reporting

Financial reporting plays a vital role in how to find net income in QuickBooks by providing a comprehensive overview of a company’s financial performance and position. These reports are used by various stakeholders, including investors, creditors, and management, to make informed decisions.

- Income Statement

The income statement summarizes a company’s revenues, expenses, and net income over a specific period of time. It is the primary report used to calculate net income in QuickBooks.

- Balance Sheet

The balance sheet provides a snapshot of a company’s assets, liabilities, and equity at a specific point in time. It is used to assess the financial health of a company and its ability to meet its obligations.

- Cash Flow Statement

The cash flow statement shows how a company generates and uses cash over a specific period of time. It is used to assess a company’s liquidity and its ability to generate cash from its operations.

- Statement of Changes in Equity

The statement of changes in equity shows how a company’s equity has changed over a specific period of time. It is used to assess a company’s profitability and its ability to attract and retain investors.

These financial reports are essential for understanding a company’s financial performance and position. By using QuickBooks to generate these reports, businesses can gain valuable insights into their operations and make informed decisions about the future.

Industry-Specific Features

Industry-specific features in QuickBooks are designed to cater to the unique accounting needs of different industries. These features streamline and simplify the process of finding net income by automating industry-specific calculations and providing tailored reports.

For instance, the construction industry often uses QuickBooks’ job costing feature to track the costs and profitability of individual construction projects. This feature helps contractors accurately determine the net income for each project, considering factors such as materials, labor, and equipment costs.

Understanding industry-specific features is crucial for businesses to find net income accurately in QuickBooks. By leveraging these features, businesses can save time and effort, improve the accuracy of their financial reporting, and gain valuable insights into their industry-specific performance.

Overall, industry-specific features play a significant role in enhancing the efficiency and accuracy of finding net income in QuickBooks. By tailoring the software to the unique requirements of different industries, QuickBooks empowers businesses to make informed decisions and optimize their financial management.

Software Updates

Software updates play a critical role in maintaining the accuracy and efficiency of QuickBooks. Regular updates provide enhancements to the software’s functionality, including improvements to the methods used for calculating net income. By incorporating the latest updates, users can ensure that their QuickBooks software is operating at its optimal level, leading to more precise net income calculations.

For instance, a recent QuickBooks update introduced a new algorithm for calculating depreciation expenses. This update improved the accuracy of depreciation calculations, particularly for assets with complex depreciation schedules. As a result, businesses using the updated software can now more accurately determine their net income, ensuring compliance with accounting standards and reducing the risk of errors in financial reporting.

Furthermore, software updates often address bugs and glitches that could potentially affect the calculation of net income. By promptly installing updates, businesses can minimize the likelihood of encountering software-related issues that could lead to inaccuracies in their financial statements. Regular updates also enhance the overall stability and performance of QuickBooks, ensuring seamless operation and reducing the risk of data corruption.

In summary, software updates are essential for maintaining the accuracy and efficiency of QuickBooks. By implementing the latest updates, businesses can take advantage of improved functionality, enhanced calculation methods, and reduced software-related errors. This ultimately leads to more precise net income calculations, ensuring reliable financial reporting and informed decision-making.

Frequently Asked Questions (FAQs)

This section addresses common questions and misconceptions surrounding the topic of “how to find net income in QuickBooks.” These FAQs aim to provide clarity and additional insights to readers seeking a deeper understanding of the subject.

Question 1: What is the most efficient way to track income and expenses in QuickBooks for accurate net income calculation?

Answer: Utilizing QuickBooks’ built-in features, such as the Chart of Accounts and memorized transactions, can significantly enhance efficiency and accuracy when tracking income and expenses.

Question 2: How does inventory management impact net income calculation in QuickBooks?

Answer: Proper inventory management is crucial as it directly affects the cost of goods sold (COGS), a key factor in determining net income. QuickBooks provides robust inventory management tools to ensure accurate COGS calculations.

Question 3: Can QuickBooks handle complex depreciation schedules for fixed assets?

Answer: QuickBooks offers flexible depreciation options, empowering users to customize depreciation schedules for various asset types, ensuring accurate and compliant net income calculations.

Question 4: How do I account for non-cash expenses, such as depreciation, in QuickBooks?

Answer: Non-cash expenses are automatically recorded in QuickBooks, ensuring a comprehensive view of expenses and their impact on net income. Users can access reports that clearly present non-cash expenses.

Question 5: What are some common errors to avoid when calculating net income in QuickBooks?

Answer: Misclassifying transactions, overlooking non-operating income/expenses, and incorrect inventory valuation methods are common pitfalls. Understanding QuickBooks’ functionality and accounting principles can help avoid these errors.

Question 6: How can QuickBooks help businesses improve their net income?

Answer: QuickBooks offers tools for financial analysis, budgeting, and forecasting, empowering businesses to identify areas for improvement, optimize operations, and ultimately increase net income.

These FAQs provide a foundation for understanding the intricacies of finding net income in QuickBooks. Delving deeper into specific aspects of income and expense management, inventory tracking, and financial reporting will further enhance your knowledge and enable you to leverage QuickBooks effectively.

In the next section, we will explore advanced techniques for optimizing net income calculations in QuickBooks.

Tips for Finding Net Income in QuickBooks

This section provides valuable tips to enhance the accuracy and efficiency of your net income calculations in QuickBooks.

Tip 1: Reconcile Bank and Credit Card Accounts Regularly

Regular reconciliation ensures all transactions are accounted for, preventing errors and discrepancies.

Tip 2: Categorize Transactions Accurately

Proper categorization of income and expenses into the correct accounts is crucial for accurate financial reporting.

Tip 3: Utilize the Chart of Accounts

Customizing the Chart of Accounts with relevant income and expense categories streamlines data entry and reporting.

Tip 4: Manage Inventory Effectively

Accurate inventory tracking ensures correct calculation of cost of goods sold (COGS), a significant factor in net income.

Tip 5: Review Depreciation Schedules

Verify and update depreciation schedules regularly to ensure accurate depreciation expense recognition.

Tip 6: Utilize Financial Reports

Generate and analyze financial reports, such as the Profit and Loss Statement, to monitor net income trends and identify improvement areas.

Tip 7: Seek Professional Advice When Needed

Consult an accountant or QuickBooks expert for guidance on complex accounting matters or industry-specific best practices.

Following these tips will significantly improve the accuracy and efficiency of your net income calculations in QuickBooks. This, in turn, provides a solid foundation for making informed financial decisions and achieving your business goals.

The concluding section of this article will delve into advanced techniques for optimizing net income calculations in QuickBooks, taking your financial management to the next level.

Conclusion

This comprehensive exploration of “how to find net income in QuickBooks” has illuminated key principles and practical approaches to ensure accurate and efficient net income calculations. By understanding the underlying concepts, leveraging QuickBooks’ features, and menerapkan the tips and techniques outlined, businesses can optimize their financial management and decision-making.

The interconnectedness of income tracking, expense classification, and inventory management is crucial in determining net income. QuickBooks provides robust tools to streamline these processes and minimize errors. Moreover, utilizing financial reports for analysis and seeking professional guidance when needed empowers businesses to identify areas for improvement and make informed choices.