Calculating loan coupon, the periodic interest payment made on a bond or loan, is a fundamental concept in finance.

In the United States, a bond with a $1000 face value and a 5% annual coupon rate pays $50 in interest each year, often in semi-annual installments of $25. Calculating loan coupon is essential for investors to determine the return on their investment and for borrowers to plan for interest payments.

This article provides a detailed guide on calculating loan coupon, including formulas, examples, and considerations for different types of loans and bonds.

How to Calculate Loan Coupon

Calculating loan coupon involves several essential aspects:

- Loan amount

- Coupon rate

- Payment frequency

- Bond maturity

- Accrued interest

- Present value

- Yield to maturity

- Discount rate

- Callable feature

These aspects are interconnected and influence the overall calculation of loan coupon. Understanding their significance and relationships is crucial for accurate coupon calculation and effective financial planning.

Loan amount

Loan amount plays a critical role in calculating loan coupon. It represents the principal amount borrowed by the borrower, which serves as the base for calculating interest payments. The loan amount directly affects the total interest expense and the overall cost of borrowing.

In a typical loan agreement, the coupon rate is expressed as a percentage of the loan amount. For instance, a loan with a $100,000 loan amount and a 5% coupon rate will have an annual interest payment of $5,000. This implies that a higher loan amount leads to a higher coupon payment, assuming the coupon rate remains constant.

Understanding the relationship between loan amount and loan coupon is essential for borrowers to plan their repayment strategies effectively. It also aids lenders in assessing the risk associated with the loan and determining appropriate interest rates. Moreover, this understanding is crucial for investors in fixed-income securities, as it helps them evaluate the potential return on their investment.

Coupon rate

In the context of “how to calculate loan coupon”, the coupon rate holds significant importance. It represents the annual interest rate or the percentage of the loan amount that is paid to the lender as interest. The coupon rate directly influences the loan coupon, which is the periodic interest payment made on a loan or bond.

- Fixed vs. Variable

Coupon rates can be either fixed or variable. Fixed coupon rates remain constant throughout the loan term, while variable coupon rates fluctuate based on market conditions or a specified benchmark. - Zero-coupon

Zero-coupon bonds are issued at a deep discount to their face value and pay no periodic interest. Instead, the investor’s return is realized when the bond matures and is redeemed at its face value. - Callable feature

Some bonds include a callable feature, which gives the issuer the option to repurchase the bond before its maturity date. This feature can impact the calculation of loan coupon, as the issuer may call the bond if interest rates fall, resulting in a lower coupon payment. - Implied coupon

Implied coupon is a measure of the yield to maturity of a bond that does not pay periodic interest payments. It is calculated using the present value of the bond’s future cash flows.

Understanding the different facets of coupon rates is crucial for calculating loan coupon accurately. It also helps investors make informed decisions when investing in fixed-income securities and enables lenders to structure loans that meet their risk and return objectives.

Payment frequency

Payment frequency is a crucial factor in calculating loan coupon. It refers to the number of times per year that interest payments are made on a loan or bond. The payment frequency directly affects the loan coupon, as it determines the interval at which interest accrues and is paid.

Most loans and bonds have a fixed payment frequency, such as monthly, quarterly, semi-annually, or annually. The choice of payment frequency is often driven by market conventions and investor preferences. More frequent payment frequencies, such as monthly or quarterly, result in smaller but more frequent interest payments. Conversely, less frequent payment frequencies, such as semi-annually or annually, lead to larger but less frequent interest payments.

Understanding the impact of payment frequency is essential for both borrowers and investors. For borrowers, it helps them plan their cash flow and ensure they have sufficient funds available to make timely interest payments. For investors, it affects the yield and return they receive on their investment. Bonds with more frequent payment frequencies tend to have lower yields compared to bonds with less frequent payment frequencies.

Bond maturity

Bond maturity, the date on which a bond’s principal amount is repaid to the investor, is a crucial factor in calculating loan coupon. It influences the frequency and amount of interest payments, the present value of the bond, and the overall return on investment.

- Term to maturity

Term to maturity refers to the number of years until a bond matures. It directly affects the frequency of interest payments and the calculation of the loan coupon. For example, a bond with a 10-year term to maturity and a semi-annual payment frequency will have 20 coupon payments.

- Maturity date

The maturity date is the specific date on which the bond’s principal amount is repaid. It is used to calculate the present value of the bond’s future cash flows, which is a key component in determining the loan coupon.

- Callable feature

Some bonds include a callable feature, which gives the issuer the option to repurchase the bond before its maturity date. This can impact the calculation of loan coupon, as the issuer may call the bond if interest rates fall, resulting in a lower coupon payment.

- Sinking fund

A sinking fund is a mechanism used by bond issuers to gradually reduce the outstanding principal amount of a bond issue. This can affect the calculation of loan coupon, as it reduces the amount of principal on which interest is paid over time.

Understanding the various facets of bond maturity is essential for calculating loan coupon accurately. It also helps investors make informed decisions when investing in fixed-income securities and enables lenders to structure loans that meet their risk and return objectives.

Accrued interest

Accrued interest, a crucial aspect of “how to calculate loan coupon,” represents the interest that has accumulated on a loan or bond but has not yet been paid to the lender or investor. Understanding accrued interest is essential for accurate loan coupon calculation and effective financial planning.

- Interest accrual period

The interest accrual period refers to the time between the last interest payment date and the current date. During this period, interest continues to accumulate on the outstanding loan balance or bond principal.

- Daily accrual

Daily accrual is the calculation of the interest earned on a loan or bond for each day within the interest accrual period. It is typically calculated as a fraction of the annual coupon rate divided by the number of days in a year.

- Accrued interest payment

The accrued interest payment represents the total interest earned during the interest accrual period that is paid to the lender or investor. It is calculated by multiplying the daily accrual by the number of days in the interest accrual period.

- Impact on loan coupon

Accrued interest can impact the calculation of loan coupon, as it is added to the regular coupon payment. This is particularly relevant when calculating the loan coupon for a bond that is purchased or sold between interest payment dates.

Accrued interest plays a significant role in ensuring accurate calculation of loan coupon and fair distribution of interest payments between borrowers and lenders. It also affects the pricing of bonds in secondary markets, as investors consider accrued interest when determining the value of a bond.

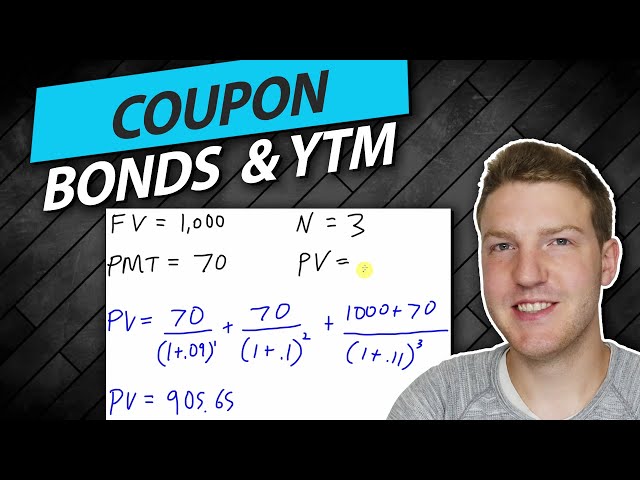

Present value

In the context of “how to calculate loan coupon,” present value plays a pivotal role in determining the worth of future cash flows. It helps assess the current value of future interest payments and the principal amount due at the loan’s maturity, providing a comprehensive view of the loan’s value.

- Time value of money

Present value considers the time value of money, recognizing that a dollar today is worth more than a dollar in the future due to its potential earning power.

- Discount rate

The discount rate, typically derived from market interest rates, is used to convert future cash flows into present value. A higher discount rate results in a lower present value.

- Future cash flows

All future interest payments and the principal repayment at maturity are discounted back to their present value to determine the overall value of the loan.

- Loan pricing and valuation

Present value is crucial for pricing loans and bonds, as it helps determine the fair value of these financial instruments based on their future cash flows.

Understanding the concept of present value and its application in calculating loan coupon empowers borrowers and lenders to make informed decisions. It enables them to evaluate the true cost of borrowing, compare different loan options, and assess the potential return on their investments.

Yield to maturity

Yield to maturity (YTM) is a crucial concept closely tied to calculating loan coupon. It represents the annualized rate of return an investor expects to receive if they hold a bond until its maturity date. Understanding YTM is vital for determining the true cost of borrowing for issuers and the potential return on investment for bondholders.

- Bond pricing

YTM is a key factor in bond pricing. Bonds with higher YTMs are generally priced lower than bonds with lower YTMs, as investors demand a higher return for taking on more risk.

- Coupon rate

YTM and coupon rate are interrelated. Bonds with higher coupon rates typically have lower YTMs, and vice versa. This is because the coupon rate represents the fixed interest payments made on the bond, while YTM reflects the overall return, including both interest payments and capital appreciation or depreciation.

- Maturity date

The maturity date of a bond also affects its YTM. Bonds with longer maturities generally have higher YTMs due to the increased risk and uncertainty associated with long-term investments.

- Market interest rates

YTM is influenced by prevailing market interest rates. When interest rates rise, bond prices fall, and YTMs increase. Conversely, when interest rates fall, bond prices rise, and YTMs decrease.

In summary, YTM is a comprehensive measure that incorporates various factors to determine the overall return on a bond investment. Understanding YTM is essential for calculating loan coupon accurately and making informed decisions in bond markets.

Discount rate

In the context of “how to calculate loan coupon,” the discount rate plays a critical role in determining the present value of future cash flows associated with a loan. It represents the rate at which future cash flows are discounted to reflect their current worth, influencing the overall calculation of loan coupon.

- Market interest rates

The prevailing market interest rates serve as a benchmark for determining the discount rate. Higher market interest rates lead to higher discount rates, resulting in lower present values for future cash flows.

- Risk assessment

The discount rate incorporates an assessment of the risk associated with the loan. Loans with higher perceived risk require a higher discount rate to compensate for the increased uncertainty.

- Maturity date

The maturity date of the loan also affects the discount rate. Longer-term loans typically have higher discount rates due to the greater uncertainty and potential for interest rate fluctuations over an extended period.

- Inflation expectations

Inflation expectations can influence the discount rate. If inflation is anticipated to be high, a higher discount rate may be used to adjust for the expected decrease in the purchasing power of future cash flows.

Understanding the various facets of discount rate is essential for calculating loan coupon accurately. By considering market interest rates, risk assessment, maturity date, and inflation expectations, lenders and borrowers can determine the appropriate discount rate to apply, leading to a fair and informed calculation of loan coupon.

Callable feature

In the context of “how to calculate loan coupon,” the callable feature offers issuers the option to redeem or “call” outstanding bonds before their maturity date. This provision significantly impacts the calculation and understanding of loan coupon.

- Call provision

The call provision defines the specific terms and conditions under which the issuer can call the bond, including the call date, call price, and any associated fees or premiums.

- Call price

The call price represents the price at which the issuer can redeem the bond. It is typically set at a premium to the bond’s face value to compensate investors for the early redemption.

- Call date

The call date specifies the earliest date on which the issuer can exercise the callable feature. This date is typically tied to specific market conditions or financial events.

- Impact on coupon calculation

The callable feature can influence the calculation of loan coupon if the issuer exercises the call option. In such cases, the loan coupon is effectively terminated or adjusted based on the call price and the remaining term of the bond.

Understanding the implications of the callable feature is crucial when calculating loan coupon. It enables investors to assess the potential risks and rewards associated with callable bonds and make informed decisions about their investments. Additionally, it helps issuers evaluate the costs and benefits of including a callable feature in their debt financing strategy.

Frequently Asked Questions about Calculating Loan Coupon

This FAQ section addresses common questions and misconceptions surrounding the calculation of loan coupon, providing clear and concise answers to help you better understand this important concept.

Question 1: What is the formula for calculating loan coupon?

Answer: Loan coupon is calculated as the annual coupon rate multiplied by the loan amount. For example, a loan with a $100,000 principal and a 5% coupon rate would have an annual coupon payment of $5,000.

Question 2: How does the payment frequency affect loan coupon?

Answer: Payment frequency determines how often interest payments are made. More frequent payments, such as monthly or quarterly, result in smaller but more frequent coupon payments. Less frequent payments, such as semi-annually or annually, lead to larger but less frequent coupon payments.

Question 3: What is the relationship between loan coupon and bond maturity?

Answer: Bond maturity, or the date when the principal is repaid, influences the frequency and amount of coupon payments. Longer-term bonds generally have higher coupon rates to compensate investors for the increased risk.

Question 4: How does accrued interest impact loan coupon calculations?

Answer: Accrued interest, or the interest earned but not yet paid, is added to the regular coupon payment when calculating the total coupon payment. This is important when purchasing or selling bonds between interest payment dates.

Question 5: What role does the present value play in loan coupon calculation?

Answer: Present value considers the time value of money and is used to determine the current worth of future coupon payments and the principal repayment at maturity. This helps assess the overall value of the loan.

Question 6: How can I calculate the yield to maturity (YTM) of a loan?

Answer: YTM is the annualized rate of return an investor expects to receive if they hold a bond until maturity. It is calculated using the present value of future cash flows and considers factors such as coupon rate, maturity date, and market interest rates.

These FAQs provide a solid foundation for understanding the key aspects of calculating loan coupon. For a deeper dive into this topic, the following sections will explore advanced concepts and practical applications.

Transition to the next article section: Exploring advanced techniques and real-world applications of loan coupon calculation.

Tips for Calculating Loan Coupon

This section provides practical tips to help you accurately calculate loan coupon and make informed decisions. By following these tips, you can ensure that your loan coupon calculations are precise and aligned with your financial objectives.

Tip 1: Determine the loan amount and coupon rate clearly.

Tip 2: Consider the payment frequency and its impact on the coupon amount.

Tip 3: Calculate the number of coupon payments based on the bond’s maturity date.

Tip 4: Account for accrued interest when purchasing or selling bonds between interest payment dates.

Tip 5: Use accurate discount rates to determine the present value of future cash flows.

Tip 6: Consider the callable feature and its potential impact on loan coupon calculations.

Tip 7: Understand the relationship between loan coupon and yield to maturity (YTM).

Tip 8: Utilize financial calculators or spreadsheets to simplify and verify your calculations.

By applying these tips, you can improve the accuracy and efficiency of your loan coupon calculations, leading to better decision-making and financial planning.

Transition to the conclusion: These tips provide a practical framework for calculating loan coupon, empowering you to make informed financial decisions and navigate the complexities of debt financing.

Conclusion

This article has provided a comprehensive guide on how to calculate loan coupon, exploring various aspects that influence its determination. By understanding the concepts of loan amount, coupon rate, payment frequency, bond maturity, and present value, individuals can accurately calculate loan coupon and make informed decisions when it comes to debt financing.

Two key points to remember are: firstly, the relationship between loan coupon and yield to maturity (YTM) is crucial, as YTM reflects the overall return on a bond investment, including both interest payments and capital appreciation or depreciation. Secondly, the callable feature can impact loan coupon calculations if the issuer exercises the call option, which should be considered when evaluating callable bonds.

Calculating loan coupon is essential for both borrowers and investors to assess the cost of borrowing, potential return on investment, and overall financial implications. By following the tips outlined in this article and gaining a thorough understanding of the subject matter, individuals can navigate the complexities of debt financing with confidence.