Bank discount, a financial concept, refers to the deduction of interest from the face value of a loan at the time of disbursement.

Understanding how to calculate bank discount is crucial for businesses and individuals seeking loans, as it impacts the overall cost of borrowing. It involves determining the present value of a future sum, taking into account the interest rate and the loan’s duration.

Knowing how to calculate bank discount empowers borrowers with the ability to assess loan offers critically, ensuring they make informed decisions. Historically, bank discounts played a significant role in the development of modern banking practices.

How to Calculate Bank Discount

Calculating bank discount accurately involves considering several key aspects. These aspects encompass various dimensions of the concept, affecting the overall calculation and its implications.

- Loan Amount

- Interest Rate

- Loan Duration

- Discount Rate

- Present Value

- Future Value

- Maturity Date

- Discount Period

Understanding these aspects is crucial for businesses and individuals seeking loans, as they impact the overall cost of borrowing. By carefully considering each aspect during the calculation process, borrowers can assess loan offers critically and make informed decisions that align with their financial objectives.

Loan Amount

Loan amount is a fundamental aspect in calculating bank discount, directly influencing the overall cost of borrowing. It represents the principal sum borrowed from a financial institution and serves as the basis for calculating interest charges and discounts.

- Principal Amount

The primary portion of the loan amount, excluding any interest or fees. - Loan Term

The duration of the loan, typically expressed in months or years, over which the borrower repays the loan. - Interest Rate

The percentage charged by the lender for borrowing the money, usually expressed as an annual percentage rate (APR). - Discount Rate

The rate used to calculate the bank discount, which may differ from the interest rate.

Understanding the interrelationship between loan amount and these other factors is crucial for accurately calculating bank discount. By carefully considering each aspect, borrowers can assess loan offers critically and make informed financial decisions.

Interest Rate

Interest rate is a pivotal aspect in calculating bank discount, directly influencing the overall cost of borrowing. It represents the percentage charged by a financial institution for the use of borrowed funds, and understanding its components is crucial for making informed financial decisions.

- Nominal Interest Rate

The stated or quoted interest rate on a loan, before considering the effects of compounding. - Effective Interest Rate

The actual interest rate earned or paid over a specific period, taking into account the effect of compounding. - Annual Percentage Rate (APR)

A standardized measure of the cost of borrowing that includes both interest and certain fees, expressed as an annual rate. - Discount Rate

The interest rate used to calculate the bank discount, which may differ from the interest rate charged on the loan.

Accurately calculating bank discount requires careful consideration of these various interest rate components. By understanding how each facet impacts the overall cost of borrowing, borrowers can critically assess loan offers and make informed financial decisions that align with their objectives.

Loan Duration

Loan duration, a critical component of calculating bank discount, significantly impacts the overall cost of borrowing. It represents the length of time over which a loan is to be repaid, influencing both the total interest charges and the discount applied.

The relationship between loan duration and bank discount is directly proportional. A longer loan duration generally results in a higher bank discount, as the lender assumes more risk by extending the loan period. This is because the lender has to account for the time value of money, which reflects the potential earnings on the funds if they were invested elsewhere during the loan duration.

In practice, loan duration plays a vital role in determining the affordability of a loan. For example, a shorter loan duration may result in a lower bank discount but higher monthly payments, while a longer loan duration may lead to a higher bank discount but lower monthly payments. Therefore, borrowers should carefully consider the trade-off between loan duration and total borrowing costs when evaluating loan options.

Discount Rate

In calculating bank discount, the discount rate holds significant importance. It influences the overall cost of borrowing and is a key factor in determining the present value of a future sum.

- Federal Funds Rate

Set by the central bank, this rate affects the cost of borrowing for banks and, consequently, the discount rate offered to borrowers.

- Prime Rate

A benchmark interest rate set by banks, it serves as a reference point for determining the discount rate for various types of loans.

- Creditworthiness of the Borrower

The borrower’s credit history, income, and debt-to-income ratio influence the discount rate offered by lenders.

- Loan-to-Value Ratio (LTV)

The ratio of the loan amount to the value of the underlying asset, it affects the risk assessment and, subsequently, the discount rate.

Understanding these facets of the discount rate enables borrowers to make informed decisions when evaluating loan offers. By considering the interplay between these factors and the broader context of “how to calculate bank discount,” borrowers can assess the true cost of borrowing and choose the option that best aligns with their financial goals.

Present Value

Present Value (PV) plays a pivotal role in “how to calculate bank discount,” as it represents the current worth of a future sum, discounted at a specific rate over a defined period. This concept is central to understanding the time value of money and its impact on the overall cost of borrowing. Bank discount, in essence, is the difference between the face value of a loan and its present value.

To calculate bank discount, one needs to determine the present value of the future loan payments, which involves considering factors such as the loan amount, interest rate, and loan duration. By discounting future payments back to the present, borrowers can assess the true cost of borrowing and compare loan offers effectively.

In real-world applications, understanding present value is crucial in various financial scenarios, including loan analysis, investment planning, and project evaluation. For example, businesses use present value to determine the net present value (NPV) of investment projects, helping them make informed decisions about capital allocation and resource utilization.

In summary, present value is a critical component of “how to calculate bank discount,” providing a framework for evaluating the time value of money and the overall cost of borrowing. By understanding the relationship between present value and bank discount, borrowers and financial professionals can make informed decisions, optimize financial outcomes, and navigate complex financial landscapes effectively.

Future Value

In the context of “how to calculate bank discount,” Future Value (FV) holds significance as it represents the value of a sum of money at a future date, considering the effects of compounding interest and inflation. Understanding FV is essential for accurately determining the present value of a loan and, subsequently, the bank discount.

- Nominal Future Value

The future value of a sum, assuming no compounding of interest over the specified period.

- Real Future Value

The future value of a sum, taking into account the impact of inflation and the decrease in the purchasing power of money over time.

- Effective Future Value

The future value of a sum, considering the effect of compounding interest over the specified period.

- Annuity Future Value

The future value of a series of equal payments made at regular intervals over a defined period.

In calculating bank discount, the future value of the loan amount is discounted back to the present using an appropriate discount rate to determine its present value. This process enables borrowers to assess the true cost of borrowing and compare different loan options effectively. Furthermore, understanding future value is crucial in various financial contexts, including investment planning, retirement planning, and project evaluation, as it provides insights into the potential growth and value of money over time.

Maturity Date

In the context of “how to calculate bank discount,” Maturity Date holds notable significance as it determines the endpoint of the loan period and serves as a crucial factor in calculating the present value and, subsequently, the bank discount.

- Loan Term

The duration of the loan, typically expressed in months or years, which directly influences the maturity date and the calculation of bank discount.

- Repayment Schedule

The agreed-upon frequency and timing of loan repayments, whether monthly, quarterly, or annually, impact the calculation of the present value based on the maturity date.

- Interest Accrual and Payment Timing

The manner in which interest is accrued and paid, whether simple or compound interest, affects the calculation of the present value and, consequently, the bank discount.

Understanding the implications of Maturity Date in “how to calculate bank discount” allows borrowers to accurately assess the cost of borrowing and make informed financial decisions. By considering the interplay between maturity date, loan term, repayment schedule, and interest accrual, borrowers can optimize their borrowing strategy and effectively manage their financial obligations.

Discount Period

In the realm of “how to calculate bank discount,” Discount Period emerges as a critical component, directly impacting the overall calculation and its implications for borrowers. It represents the duration over which the discount is applied to the face value of a loan, shaping the effective cost of borrowing.

The Discount Period directly influences the present value of the loan, which is the cornerstone of calculating bank discount. A longer Discount Period reduces the present value of future payments, leading to a lower bank discount. Conversely, a shorter Discount Period results in a higher present value and, consequently, a higher bank discount. Understanding this relationship empowers borrowers to evaluate loan offers critically and assess the true cost of borrowing, enabling informed financial decision-making.

In practice, Discount Period plays a crucial role in various financial scenarios. For instance, in invoice discounting, businesses leverage their unpaid invoices to secure financing, with the Discount Period determining the duration over which the discount is applied. Similarly, in trade discounting, manufacturers offer discounts to retailers for purchasing in bulk, where the Discount Period influences the effective cost of goods for the retailer. By comprehending the impact of Discount Period, businesses can optimize their financial strategies, manage cash flow effectively, and navigate complex lending landscapes.

In summary, Discount Period stands as a fundamental aspect of “how to calculate bank discount,” influencing the present value of future payments and ultimately shaping the cost of borrowing for individuals and businesses. Grasping the connection between Discount Period and bank discount empowers stakeholders to make informed financial choices, optimize their borrowing strategies, and achieve their financial objectives.

Frequently Asked Questions

This section addresses common queries and clarifies aspects of “how to calculate bank discount,” providing concise and informative answers to guide your understanding.

Question 1: What is bank discount, and how does it differ from interest?

Bank discount refers to the deduction of interest from the face value of a loan at the time of disbursement, while interest is typically charged over the loan’s duration. Bank discount represents the present value of future interest payments.

Question 2: What factors influence the calculation of bank discount?

The calculation of bank discount primarily involves the loan amount, interest rate, loan duration, and discount rate, among other factors.

Question 3: How does the discount rate impact bank discount?

The discount rate, which may differ from the interest rate, is used to determine the present value of future loan payments, directly influencing the amount of bank discount.

Question 4: What is the relationship between the loan duration and bank discount?

Generally, a longer loan duration results in a higher bank discount, as the lender assumes more risk by extending the loan period.

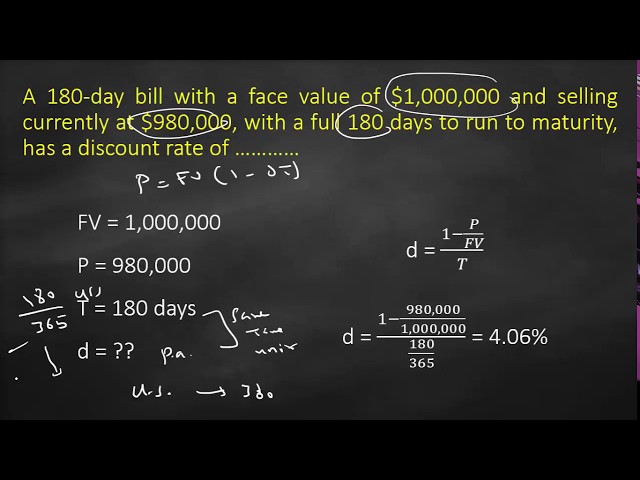

Question 5: How is bank discount calculated?

Calculating bank discount involves determining the present value of future loan payments using the formula: Bank Discount = Face Value – Present Value of Loan Payments.

Question 6: What are the implications of bank discount for borrowers?

Understanding bank discount empowers borrowers to assess loan offers critically, compare the true cost of borrowing, and make informed financial decisions.

These FAQs provide a strong foundation for comprehending “how to calculate bank discount.” For further insights and practical applications, let’s explore additional aspects of this topic.

Transitioning to the next section, we will delve deeper into the significance of bank discount, its advantages, and considerations for effective utilization.

Tips for Effective Bank Discount Calculation

Understanding how to calculate bank discount is crucial for informed financial decision-making. Here are some actionable tips to guide you:

Tip 1: Determine Loan Parameters

Clearly identify the loan amount, interest rate, loan duration, and discount rate to ensure accurate calculation.

Tip 2: Calculate Present Value

Utilize the present value formula to determine the current worth of future loan payments, considering the time value of money.

Tip 3: Apply Bank Discount Formula

Employ the formula Bank Discount = Face Value – Present Value of Loan Payments to calculate the bank discount.

Tip 4: Compare Loan Options

Calculate and compare bank discounts for different loan offers to identify the most favorable option.

Tip 5: Consider Loan Duration

Evaluate the impact of loan duration on bank discount, as longer durations generally result in higher discounts.

Tip 6: Assess Discount Rate

Understand how the discount rate influences the calculation and its implications for the overall cost of borrowing.

Tip 7: Consult Financial Advisor

Seek professional guidance from a financial advisor to optimize your bank discount calculations and make informed decisions.

Summary: By following these tips, you can accurately calculate bank discount, empowering you to make well-informed borrowing choices and manage your finances effectively.

In the concluding section, we will explore advanced strategies for leveraging bank discount to maximize financial benefits and minimize borrowing costs.

Conclusion

Throughout this exploration of “how to calculate bank discount,” we have gained valuable insights into its significance and implications. Understanding the calculation process empowers borrowers to assess and compare loan offers critically, enabling informed financial decision-making.

Key points to remember include:

- Bank discount represents the deduction of interest from the face value of a loan at the time of disbursement, influencing the overall cost of borrowing.

- Calculating bank discount involves determining the present value of future loan payments using the discount rate, providing a comprehensive view of the loan’s cost.

- Effective utilization of bank discount requires careful consideration of factors such as loan amount, interest rate, loan duration, and discount rate, ensuring optimal financial outcomes.

In summary, understanding “how to calculate bank discount” is an essential skill for managing finances effectively. By leveraging the insights gained from this discussion, individuals and businesses can navigate lending landscapes with confidence, making informed choices, and maximizing financial benefits.